How Do Corporate or B2B Payments Work? A Guide to AP, Treasury Flows, and More

We all make payments and transact as consumers on a daily basis. Corporate payments are how businesses move money, though they take place behind the scenes and matter mostly to finance and treasury professionals. Nevertheless, every company must pay and get paid while managing the complexity of doing both at scale.

Most of the time, businesses tend to focus more on incoming revenue than on outgoing payments. Recently, though, there has been a shift as companies prioritize becoming leaner, more efficient, and better at preserving cash. The technology available is also improving: new software solutions have emerged, banks are modernizing, and real-time payment systems are gaining adoption.

An optimized payment process can help reduce manual work, minimize errors and security risks, and cut unnecessary costs. It can also be crucial for maintaining healthy cash flow. Better payment terms help keep cash within the business for longer, scheduling payments to align with cash inflows ensures liquidity, and greater visibility allows for more precise reporting and forecasting.

Payment capabilities are fully integrated into the Atlar treasury platform. We help finance teams at companies like Aiven, Liberis, and Zilch to centralize and secure payments through two-way connections with their banks and ERP systems – often with dramatic results. The team at Loomis Pay saves 120 hours of work each week by streamlining accounts payable with Atlar, for example.

What are corporate or B2B payments?

Corporate or business-to-business (B2B) payments are payments made by a business entity. These payments can be made to other businesses, such as suppliers or software vendors, to other entities within the same group, to governmental authorities, or to individuals. The main types of corporate payments are treasury payments, accounts payable (AP) or supplier payments, tax payments, and salary payments.

These payments are often handled by different teams: the accounts payable team handles supplier payments, while HR manages salaries. At international companies, responsibility may be spread across several local entities. Given their business-critical nature, finance teams are often tasked with overseeing these payments centrally to ensure that appropriate processes and controls are in place, reducing costly errors and preventing possible fraud.

Businesses are making an increasing number of these payments each year. By 2027, the average mid-sized business will make over 1,400 domestic payments, along with a similar number of cross-border transactions. Several trends are driving this growth: the diversification of supply chains and supplier networks; the shift toward just-in-time inventory management; the rise in outsourcing and cloud-based SaaS adoption; and that more companies are ‘born global’ from the outset.

How do corporate payments differ from consumer payments?

Most of the innovation in payments over the last few decades has focused on consumer payment flows. New technologies like instant payments, mobile wallets, and account-to-account or open banking payments have helped to make payments easier and faster for consumers.

Meanwhile, corporate payments have lagged behind. Many companies still rely on older, legacy systems and a sizable portion of payments are not processed using any software at all. In 2022, paper checks were used for around 31% of all corporate payments globally.

Several factors have led to this relative lack of innovation. Corporate payments are more complex and involve much higher transaction values. There are regulatory and tax requirements to consider, and they often occur in the context of business relationships, negotiated contracts, and variable payment terms.

In the last few years, though, there has been a noticeable uptick in the number of new digital payment technologies aimed at businesses and corporate finance teams are placing greater emphasis on optimizing their payment processes than ever before.

Transaction size and complexity

The total value of payments made by businesses far exceeds that made by consumers. Corporate payments amount to around $124 trillion per year globally, more than double the total value of payments initiated by consumers, primarily because the average value of a transaction is much higher.

Corporate payments are also fundamentally more complex than consumer payments, which involve the direct purchase of goods or services for a fixed, non-negotiable price. Corporate payments can involve bulk purchases, recurring payments for services, and the need for detailed invoicing and purchase orders. They can also vary in terms of the payment duration, discounts, and delivery timelines.

Reliability, security, and compliance

While consumer payments are optimized for convenience and speed, reliability and security are key to corporate payments. This is because of the much larger transaction values, the importance of supplier relationships, and the greater impact of payment errors or fraud on business operations.

Corporate payments often occur in the context of business relationships, negotiated contracts, and custom terms of service. This dynamic adds to the need for reliability in order to adhere to contract laws and maintain a positive relationship with business partners. They are also subject to more complex regulatory, compliance, and tax obligations which vary by country or region. This means companies require detailed invoicing, accurate accounting records, and audit trails for each transaction.

Payment methods and processing

Corporate payments are typically made through bank transfers, which come in several different forms, along with non-digital methods like checks and newer real-time payment options. A key difference between corporate and consumer payments is the payment terms. Corporate payments typically have longer payment periods, such as 30 or 60 days, while consumer payments are expected to be immediate.

Given the added complexity, the end-to-end process for corporate payments involves several steps and can result in a significant amount of administrative work for finance teams if not managed properly. This does, however, create opportunities to optimize the process to your benefit – covered in more detail below.

The corporate payment cycle

The corporate payment cycle is the process that businesses follow when making a payment, starting from issuing a purchase order to final reconciliation. It applies especially to accounts payable (AP) or supplier payments but certain steps apply to other payment types too. Here is an example of a typical process:

- Creation of a purchase order (PO): The process starts when the buyer prepares and sends a purchase order to the seller outlining the requested goods or services, quantities, pricing, and agreed-upon payment terms. It acts as a formal offer to purchase.

- Confirmation and invoice preparation: The seller confirms their ability to fulfill the PO and issues an invoice that includes details such as the amount due, terms, and payment instructions. If the seller is providing a service, this might be issued retroactively once the service has been fulfilled.

- Delivery of goods or services: The seller delivers the product or service as specified in the PO. The buyer may require documentation such as shipping receipts before releasing the payment.

- Invoice approval and payment processing: If everything is in order, the buyer approves the invoice for payment. In larger companies, this can be a multi-step approval process across various departments, such as procurement and finance. Any issues may lead to returns or disputes.

- Payment execution: The buyer processes the payment using the chosen method. To do so, they might enter the payment in their corporate banking portal or use specialized software, such as an AP automation tool.

- Payment tracking and confirmation: After processing the payment, the buyer may monitor its status to ensure successful execution and avoid potential late fees or relationship damage. Once the seller receives the payment, they provide confirmation to the buyer. Any errors or disputes during the payment cycle may require the payment to be retried or returned.

- Reconciliation: Both the buyer and seller must reconcile the payment with their financial records. This involves verifying that the purchase order (PO) details, such as the amount and reference number, match those on the invoice and in the transaction shown on their respective bank statements. If these records do not align, a manual investigation will be needed.

- Reporting and analysis: Both the buyer and seller may include the transaction in their cash reporting and forecasting for analysis. These reports are valuable for cash positioning – understanding the company's current cash status – and for predicting short-term cash flow.

- Recordkeeping and compliance: Throughout the payment cycle, both businesses maintain detailed records of all documents, including POs, invoices, payment confirmations, and any correspondence, to meet legal, tax, and compliance requirements.

Main types of corporate payments

Treasury payments

Treasury payments are a subset of corporate payments that are made as part of a company’s treasury management activities. This includes both day-to-day cash management and more strategic activities aimed at controlling liquidity, funding, and financial risk. Treasury payments are typically controlled by a company’s treasury department.

Transaction types

Depending on a company’s financial situation and treasury strategies, it will need to manage, initiate, and track payments for some or all of these transaction types:

- Repaying loans

- Servicing debt

- Managing margin requirements for hedges and other financial instruments

- Settling hedges, such as options or forwards

- Managing currency exposure, including payments for foreign currency conversions

- Investing surplus cash into short-term or long-term investments

- Settling corporate finance deals

- Coordinating intercompany payments to manage funds between different entities or as part of a cash pooling strategy

How to manage treasury payments

Treasury payments can range from simple recurring interest payments to more complex transactions, such as settling the cash consideration for closing an M&A deal. Improper management of these payments can lead to serious negative outcomes, given the financial risks involved.

A common type of treasury payment is an intercompany transaction between different entities within the same group, often carried out as part of a cash pooling strategy to maintain sufficient liquidity across the group and consolidate cash for higher-return investments. Atlar enables automated sweeping workflows for exactly this purpose, helping customers to manage liquidity with ease.

Given the risks and large transaction values involved, treasury payments should be handled by the treasury team or individuals with specialized training, and ideally using a treasury management system or similar. Such systems provide features like approval chains, role-based access controls, and audit trails that are essential to managing complex financial transactions in a compliant way.

Accounts payable

Accounts payable refer to the money a company owes to suppliers, vendors, or contractors for goods or services that have been received but not yet paid for. A payable is essentially a short-term ‘IOU’ from one business to another, which the counterparty enters in its own records under accounts receivable (AR).

An account payable (AP) payment refers to the actual payment of an unpaid ‘IOU’ or invoice, which usually have payment terms of 30, 60, or 90 days. Typically, the longer the payment term the better, as that improves working capital in the short term.

Managing AP processes and payments is a critical element in controlling a company’s short-term cash flow. Unlike accounts receivable, which depend on when a customer or client decides to pay you, accounts payable are within the company's direct control, as it ultimately decides when to make payments.

If accounts payable increase over time, it means the company is buying more goods or services on credit, rather than paying cash upfront. This could improve working capital in the short term, but only if the company manages its payables efficiently and is certain to meet these obligations when they become due. This balancing act is part of managing a company’s working capital cycle, meaning the time it takes for a business to convert its current assets and liabilities (working capital) into cash.

AP automation software can be used to simplify the AP payment cycle, from scanning invoices and capturing transaction details to facilitating reconciliation. These systems typically do not handle the actual execution of a payment, which requires integrations with a company’s banking partners.

Transaction types

AP payments are made for any goods or services purchased from a supplier, vendor, or contractors. In terms of their accounting treatment, there are three categories of accounts payable:

- Trade payables: payments owed for inventory purchases that are recorded at the time of purchase or when the inventory is received

- Expense payables: payments owed for operational expenses (such as utilities, rent, and professional fees) that are recorded upon receipt of the invoice

- Accrued expenses: expenses that have been incurred (and entered into the books) but not yet invoiced

AP payments can be made by several different methods depending on the supplier or vendor. Some common examples of AP payments are:

- Supplier invoices

- Legal fees

- Contractor payments

- Travel expenses

- Equipment and software purchases

How to manage AP payments

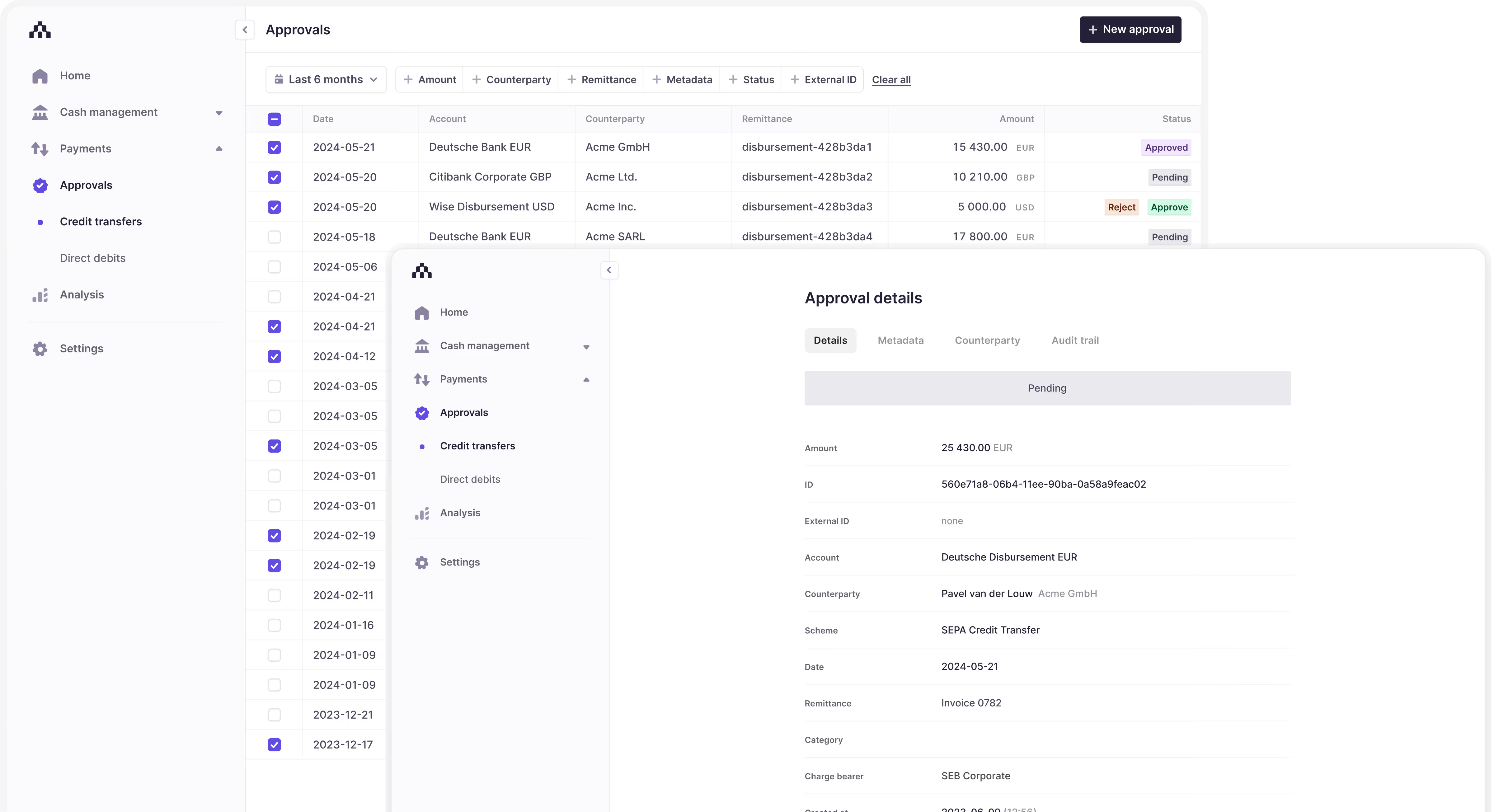

The execution of an AP payment is a critical step in managing the end-to-end AP process. Operationally, AP payments can be automated through an integration with a company’s ERP system. For example, Atlar enables companies to process AP payments from inside their ERP, such as NetSuite or Dynamics 365, and send these for payment in bulk through Atlar to their banking partners. This lets companies automate AP processes at scale with full bank-ERP syncing and a high degree of internal control.

The alternative to using bank-ERP connections to automate AP payments is making each payment individually in online banking portals or by manually uploading payment files. This can be time-consuming and prone to error, and may fall short of compliance requirements. Platforms like Atlar remove these headaches by enabling payments to be made from one central interface with built-in payment templates and counterparty management.

Given that AP payments are often made by different teams, they can be difficult to coordinate and oversee centrally. Lacking a proper approval system, AP payments are prone to manual errors and an increased risk of compliance breaches and potential fraud. Conversely, centralizing responsibility in a single team or individual creates key-person dependencies, delays, and an increased risk of late payments – potentially disrupting operations and damaging supplier relationships.

Using a treasury platform like Atlar with robust user management features, full audit trails, and built-in approval chains can help companies get around this dilemma. You can restrict team members’ access to specific banks and payment types and ensure that payments above a certain threshold require approval. These measures enable teams to collaborate securely and efficiently when it comes to AP payments.

Tax payments

Next to treasury and AP payments, tax payments are one of the most common types of corporate payments. These are payments made to tax authorities to fulfill a company's legal tax obligations and are a crucial part of a company's operations. Failing to make them for any reason can lead to significant legal and financial repercussions, including costly penalties and a loss in standing with financial authorities.

Transaction types

The nature of a company’s tax payments depends on the tax jurisdictions in which it operates. Tax systems are designed, administered, and enforced by national governments, though many countries have tax laws that require corporations to pay taxes on their worldwide income, regardless of where the income is earned. Some of the common types of tax payments include:

- Income tax

- Sales tax

- Property tax

- Corporate tax

- Tariffs on imported goods

How to manage tax payments

Tax payments are usually managed by qualified tax experts. In-house teams are more common at larger companies while smaller businesses may use an external accounting firm or tax advisors. Companies may also use tax software that integrates with their ERP, accounting system, and treasury management system in order to align tax payments with their cash flow cycles to maintain liquidity.

Salary payments

Salary payments are the compensation a company provides to its employees under agreed-upon terms in exchange for their job performance. This includes not only salaries and wages but also bonuses and benefits. They are a major cash flow component and often represent a significant portion of a company’s operating expenses.

Transaction types

Salary payments can be categorized based on their nature, purpose, and the way they are calculated. Below are the main types:

- Base salary

- Hourly wages

- Overtime pay

- Bonuses, incentives, and benefits

- Equity compensation

- Paid time-off (e.g. vacation, sick leave)

How to manage salary payments

Making salary payments on time and in the correct amounts is key for reducing employee turnover, preserving the company’s reputation, and avoiding any disruption to business operations.

These payments are often a predictable, recurring expense that allows for accurate forecasting and budgeting. They can be included in both shorter-term treasury forecasts (typically with a 13-week time horizon) and long-term cash budgeting, where considerations should include salary increases, hiring plans, and potential bonuses.

Atlar offers built-in cash flow forecasting for up to 13 weeks into the future, with data synced from your banks and ERP. Upcoming salary payments can be automatically categorized and fed into your forecast from your accounting records. You can also input data manually to update your forecast in real time, helping you assess the impact of changes in headcount or compensation levels.

Many companies also implement a payroll management system to automate salary calculations, deductions, and payments. These systems can often be integrated with your ERP to ensure your accounting records are kept up-to-date automatically.

Types of corporate payment methods

Corporate payments can be made through various methods such as cash, checks, bank payments or transfers, and credit cards. Today they are typically processed electronically through banks, though checks are still widely used in the U.S. and some other countries. In a 2022 survey, the Association for Financial Professionals (AFP) found that 73% of companies have plans to digitize all of their B2B payment processes or have already done so.

Bank payments

Bank payments are the predominant method for making corporate payments today, either as credit transfers (push-based) or direct debits (pull-based) processed electronically. These payments can be categorized as either domestic or cross-border. Cross-border payments usually involve foreign exchange risk due to currency fluctuations.

For domestic payments, there are a number of local or regional payment schemes that each follow their own rules and processing cycles. There’s ACH and Fedwire in the US, the SEPA payment schemes in Europe, and separate schemes specialized in corporate payments in countries like the United Kingdom, Switzerland, Sweden, Denmark, and many more.

Real-time payments

In the last few years, real-time or instant payments have gained traction globally as a corporate payment method. New payment systems like FedNow in the US, SEPA Instant Credit Transfer in the EU, and Faster Payments in the UK are seeing rapid growth in business usage. These schemes enable settlement in real time, 24 hours a day, 7 days a week, as opposed to batch-based settlement cycles of 2-3 business days.

At the same time, more and more banks are starting to offer proprietary APIs that provide companies with programmatic, real-time payments capabilities. Revolut is one such example, offering a premium corporate API to business customers (with which Atlar has a full integration).

In addition to the speed of payment, a key benefit of real-time payments is the ability to send and receive messages alongside funds. These data-rich messages unlock capabilities like real-time reconciliation, live status tracking, improved fraud detection, and automated processing. For more information on how this benefits companies, read our deep-dive on real-time banking APIs.

Three main ways to manage corporate payments

At scale, the processes and technology used to manage corporate payments can have a major impact on a company’s performance. Deloitte research found that it costs nearly $8 to process an AP payment manually, with 62% of that cost attributable to the time spent by the finance team. On average, it takes 30 days for a manual payment to be completed and still 47% of suppliers end up being paid late.

On top of this, companies face the ever present risk of corporate payment fraud. In an AFP survey of over 500 treasury professionals, 80% of companies reported being victims of payment fraud in 2023 – and nearly one-third were unable to recoup any of the lost funds.

Effectively managing corporate payments means minimizing the risk of fraud and errors, reducing costs, improving short-term cash flow, and ultimately ensuring the company can meet its financial obligations. It’s fair to say that finance teams have historically been underserved by software solutions in this area, but this has begun to change.

Manual payments

In a company’s early stages, corporate payments are often processed manually. While this approach may be effective for small businesses due to its simplicity and low cost, it can lead to headaches – and more seriously, operational and compliance risks – as the company grows.

On average, Atlar customers maintain relationships with five banking partners, which would lead to considerable time spent manually logging into each banking portal and entering data. Additionally, a Deloitte survey found that 22% of mid-market businesses relying on manual processes experience payment fraud, largely due to insufficient internal controls on each payment.

How it works

Managing corporate payments manually involves maintaining a spreadsheet of accounts payable which team members use to track completed payments. In order to execute a payment, you need to log into the appropriate banking portal and enter the details manually.

- Tracking accounts payable: The team compiles a list of all outstanding invoices and bills that require payment. This list is often kept in a spreadsheet or basic accounting software.

- Manually executing payments: Team members log into each banking portal individually to process payments. They manually enter payment details including counterparty information, payment amount, and any relevant references. There is typically no approval process in place.

- Recording transactions: After each payment, team members mark it as completed in the list of accounts payable in order to prevent duplicate payments. Without any tracking or status updates in place, they may have to log into each banking portal to check that the payment was successful.

- Reconciling transactions: Payments are manually reconciled using spreadsheets or accounting software. Team members compare the payments recorded in their internal lists with bank statements to ensure accuracy.

Benefits of manual payments

For many small businesses, this manual approach may make sense for three key reasons:

- Cost efficiency: Manual payment processes don’t require any investment in specialized software, helping to keep operational costs low.

- Oversight: Handling payments manually allows you to closely monitor cash outflows and identify trends and irregularities – assuming a small volume of payments.

- Simplicity: Provided you have up-to-date payment and counterparty information, making payments manually is a straightforward (if cumbersome) process that requires little formal training.

Challenges with manual payments

As a company grows, manual payments become increasingly inefficient, time-consuming, and fraught with risk to the point that they are no longer manageable. Here are some of the key pitfalls to be mindful of:

- Time consumption: A task that once took a few hours per week requires significantly more time with a larger volume of payments, diverting attention away from more strategic tasks.

- Inefficiency: Manually entering each payment is slow and can lead to delays that damage supplier relationships. Since the process isn’t scalable, companies find themselves adding more staff.

- Security risks and errors: Multiple staff members being able to access banking portals increases the risk of security breaches and unauthorized or fraudulent transactions. More manual data entry increases the risk of errors, such as duplicate or misdirected payments and incorrect amounts.

- Reconciliation: Manual reconciliation becomes more complex with higher payment volumes – often requiring data to be collected from multiple systems – and the risk of discrepancies going unnoticed is increased.

- Managing multiple banking portals: The use of multiple bank accounts requires team members, potentially in different locations, to juggle login credentials and navigate different user interfaces.

Dedicated payments tooling

As companies grow and their payment volumes increase, some organizations turn to dedicated payments software. These tools are often specialized in one area of corporate payments, such as AP automation software, payroll systems, tax compliance systems, and expense management tools.

Implementing such software offers a range of potential benefits but also introduces new processes, costs, and training requirements. Since these tools usually focus on facilitating one type of payment, such as AP payments, a company may need to use several of them. Plus, the implementation itself will need to be resourced and managed properly.

Benefits of dedicated payments tooling

- Automation: Payment software is designed to automate routine tasks such as data entry, payment initiation, and reconciliation, helping to minimize errors. It also allows you to schedule payments by setting up recurring or future-dated transactions.

- Centralized system: If the software solution offers multi-bank connectivity, payments can then be made from various bank accounts, and in multiple currencies, through one platform. This also provides a consolidated view of outgoing payments and is more scalable than manual processes.

- Improved reporting: Most payments software solutions offer reports on data gathered over the course of the payment process, as well as providing tools for auditing and monitoring.

- Security and compliance: If present, features such as multi-factor authentication, approval chains, access controls, and fraud detection can improve payment security as well as simplifying adherence to AML and KYC requirements.

- Faster processing: Dedicated software can help accelerate payment cycles, improving supplier relationships and reducing the time spent on payment processing.

Challenges of dedicated payments tooling

A dedicated payment solution offers obvious advantages over manual processing. But the process of implementing and maintaining one, especially if it is one among many other systems, can also have potential downsides:

- Implementation costs and fees: Depending on the provider and features, costs can be significant, especially for companies with more sophisticated needs. Some platforms charge per transaction, which can add up with high volumes, and customization may incur extra fees.

- Integration challenges: Any new software solution must be compatible with existing ERP, accounting, and banking systems, both now and in the future. Disconnected systems provide fewer benefits in terms of automation and reporting, often requiring manual workarounds and increasing a company’s technical debt.

- Team resources: Setting up the software requires time for configuration, testing, and integration with existing systems – this can result in significant administrative and engineering work both during implementation and future system updates.

- Training and onboarding: Adapting to new systems may require dedicated training. If the software isn’t particularly user-friendly or is one of several systems in use, it may experience lower adoption and might even necessitate a full-time staff member to operate it.

Treasury software with payment capabilities

As a company continues to grow, its financial activities often become more complex, potentially spanning multiple countries, entities, and currencies. At this stage, managing one or more specialized payment systems can become inefficient and error-prone. It involves regular manual file uploads between the system, your banks, and ERP, with data often needing to be consolidated in a spreadsheet for reporting and reconciliation.

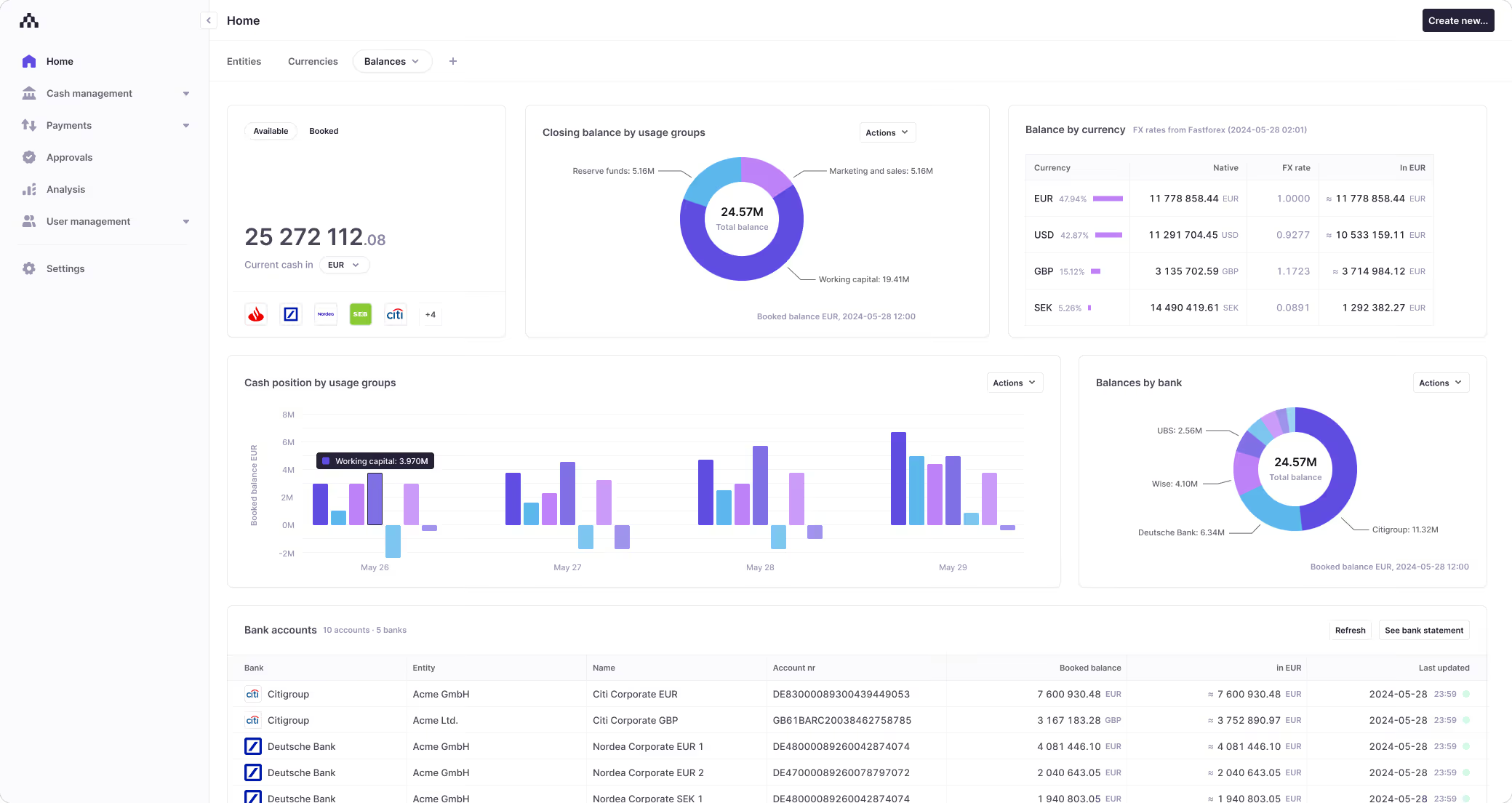

Modern treasury platforms like Atlar centralize payments and other key operations, such as cash management, reporting, and accounting, into one unified system that integrates with banks, payment platforms, and ERP systems. This makes it an appealing option for companies that have outgrown manual processes and are looking to combine payments with cash flow, liquidity, and other treasury activities.

Keep in mind that not all treasury software solutions offer integrated payment capabilities, especially those relying on open banking APIs to connect to a company's banks. Unlike corporate banking APIs and established connectivity methods such as host-to-host and EBICS, open banking can result in patchy coverage, reduced reliability, and limited functionality for corporate payments.

Benefits of treasury software

An all-in-one treasury platform with payment capabilities can offer a strategic advantage for businesses. By consolidating payments, cash management, forecasting, and accounting in a single system, companies can reduce administrative work, gain better visibility, and use cash more efficiently:

- Cost efficiency: A single platform for payment and treasury activities means fewer vendors and, ultimately, lower costs. Separate platforms, on the other hand, require individual implementation projects and must be integrated with any new software purchases, limiting their scalability.

- Simplified operations: Treasury platforms are designed to integrate with banks, centralize data, and improve bank account management. A unified interface accessible to multiple finance functions, with role-based access controls, can enhance collaboration across the team.

- Consolidated data: Having all financial data stored in one place creates a single source of truth, allowing for comprehensive reporting and analytics without the need to manually transfer data or use spreadsheets. The ability to access information faster, in one place and in real time, also enables quick and proactive decision-making.

- Compliance and risk management: A central system allows for the easier enforcement of compliance and security protocols across the entire finance organization, from approval chains to multi-factor authentication and audit trails.

Challenges of treasury software

As with any new software solution, it is crucial to choose the right treasury platform for your needs, avoiding unnecessary complexity and a long, costly implementation project.

Modern treasury platforms like Atlar combine the core functionality of a traditional treasury management system (TMS) with modern API connectivity, real-time reporting, and user-friendly tools. Quicker to implement and easier to use than legacy TMS solutions, these platforms are an attractive option for businesses with financial complexity but limited budgets for tooling and IT support.

If you’re starting to evaluate treasury software and are in need of guidance, read our deep-dive on choosing the right treasury management system.

How Atlar simplifies corporate payments

Efficient and secure payment handling is a cornerstone of every high-functioning finance team. While dedicated payment platforms improve on manual processes, they present challenges for future scalability, such as increased complexity, higher costs, ongoing training, and added technical debt.

The Atlar platform helps you modernize the way you manage payments while supporting a wide range of other operations in one system, from accounting to cash flow analysis and bank account management – all through a single, comprehensive interface that the entire team can use.

The team at Tibber switched from manual payment processes and legacy banking interfaces to using Atlar for corporate payments, saving 50 hours per month for a lean finance team. Below are some of the ways Atlar helps Tibber and finance teams at GetYourGuide, Acne Studios, and many others to centralize and streamline their payments.

Best-in-class bank connectivity

Reliable bank connections are integral to well-managed corporate payments. Atlar’s platform offers direct, fully managed connections to over 40 major banks and counting, plus a number of key payment providers, expense management tools, and more. This lets you centralize all payments in one place, avoiding the need to log into multiple banking portals, transfer files to and from your ERP, and export data into spreadsheets.

While some treasury systems specialize in a single connection type or rely on open banking APIs with limited payment coverage, Atlar supports both established methods like host-to-host and EBICS, as well as real-time corporate banking APIs. This flexibility allows you to leverage the best-performing connection type for each bank, ensuring payments are executed securely and as quickly as possible, while also benefiting from API-based features like real-time status updates and automated retries.

Atlar also builds and manages all bank connections on behalf of its customers, potentially equating to hundreds of hours saved and delivering significantly quicker implementations – without any consultants, implementation work, or additional fees.

Centralized payments dashboard

By seamlessly integrating bank and ERP data in one place, Atlar removes the need to navigate between multiple systems, transfer files, and manually enter payment details. Through our native integrations with ERP systems like Oracle NetSuite and Microsoft Dynamics 365, customers can trigger payment runs with a click and automatically sync bank statements back to their ERP.

Atlar acts as a central source of truth for payment processing and reporting. Using built-in analytics tools, this lets you quickly create cash flow reports or forecasts using the latest, most accurate data from your banks and ERP system. Additionally, detailed transaction information is just one click away, providing quick access to payment details for swift issue resolution and greater transparency across all payment activities.

Multiple payment options

Atlar supports various types of credit transfers and direct debits over multiple local schemes, enabling seamless transactions across different regions. Payments can be initiated manually on an ad hoc basis prebuilt payment templates and auto-filled counterparty details, in bulk using file uploads, programmatically over API, or from inside your ERP system.

This enables you to centralize all payments in one platform, enforcing proper checks and controls on every payment while automatically standardizing the data for use in reporting. And with all bank accounts connected to Atlar, you can easily make internal transfers between accounts for efficient cash management and set up automated sweeping workflows, facilitating your cash pooling strategy.

Enhanced security and compliance

A secure, error-free payment process is non-negotiable for most growing companies. Atlar's modern treasury platform strengthens payment security and compliance without compromising speed or ease-of-use. Customizable approval chains ensure that every payment is properly reviewed and complies with internal policies such as the four-eyes principle, while granular user management controls let you dictate who can access what based on predefined roles, preventing unauthorized activity.

Additionally, customers can leverage payment templates to standardize recurring transactions, minimizing errors, and Atlar’s counterparty management features let you securely store recipient details to further reduce errors and avoid misdirected payments. Secure authentication methods, like multi-factor authentication (MFA) and single sign-on (SSO), add an extra layer of prevention against possible fraud, while accounting teams can leverage immutable audit trails for a detailed record of all actions, ensuring full transparency.

See a modern treasury platform in action

If your company is exploring ways to improve its payment processes, talking to our team is a great place to start. Book a 30-minute demo to discuss best practices and see Atlar’s payment capabilities in action.

You can unsubscribe anytime.

Most recent

See Atlar in action.

Enter your work email to watch a live product demo.