Bank-ERP Connectivity: How to Automate Statement Feeds and Payment Runs

ERP systems have long been a core piece of infrastructure for mid-market and scale-up companies. ERPs like Oracle NetSuite bring together data from multiple functions: accounting, supply chain, HR, and CRM. For financial operations, there’s another data source that’s just as important: a company’s banking partners. Combined with the ERP, they’re the two key pillars of all financial data and processes.

On the ERP side, you have the internal record of business transactions, covering everything from accounting entries and invoices to procurement, payroll, and inventory. Meanwhile, the bank is the source of all cash movement—incoming payments from customers, outgoing payments to suppliers or employees, intercompany transactions, and all cash balances.

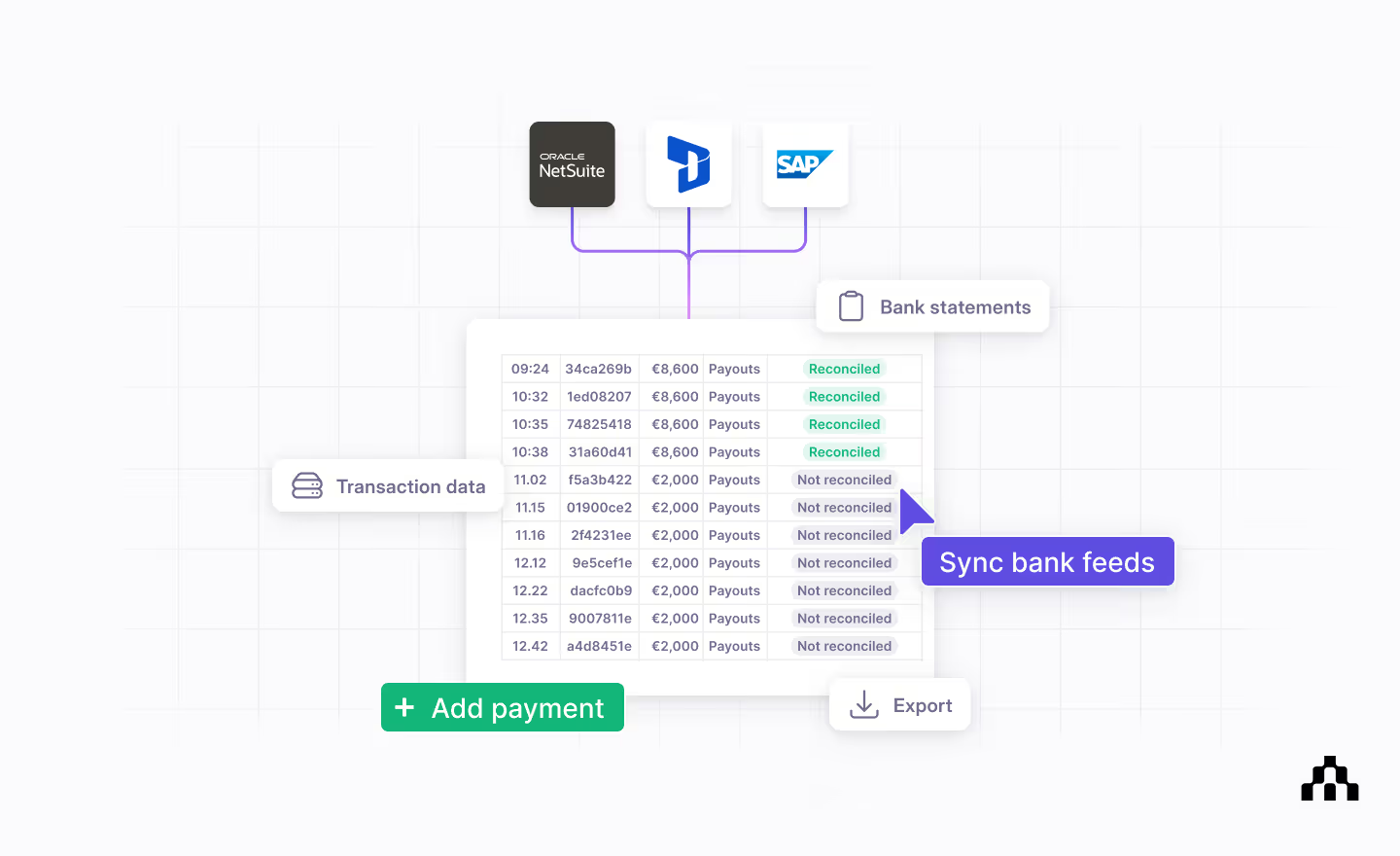

Bank-ERP connectivity is the direct link between a company’s ERP system and its banks. With an automated connectivity solution in place, statements and balances flow from the bank to the ERP, and payment or collection instructions flow from the ERP back to the bank. Previously, we looked at bank connectivity on its own—this post covers the value of connecting ERPs to the flow of data and how companies can make it happen.

At Atlar, we have a fair amount of experience in multi-bank and ERP setups. We work with finance teams at customers like Zilch, Aiven, Upvest, and Liberis to securely connect their banks and ERP for seamless bank feeds and payment runs. If you're interested in a free, 30-minute consultation with one of our experts, get in touch.

Why integrating banking and ERP systems is critical

For most companies that reach a certain size and degree of financial complexity, a reliable bank-ERP integration becomes non-negotiable. When the two main data sources—banks and the ERP—operate in isolation, finance and treasury teams face significant friction.

Five signs it’s time to connect your banks and ERP

When a company spans multiple subsidiaries (potentially transacting in different currencies) and uses more than one bank (holding numerous accounts across them), the lack of bank-ERP connectivity can be painful and may even result in reputational or regulatory risks.

- Multiple subsidiaries or business units: Once a company is managing several legal entities or brands, integration keeps each subsidiary’s finances transparent and standardized.

- Regional or global expansion: Operating in multiple currencies introduces FX risk and reconciliation issues; ERP-bank integrations centralize this data and automate conversion.

- High transaction volume: If payment runs or incoming cash transactions grow into the hundreds per month, manual approaches become unsustainable. Without a bank-ERP integration, payment approvals happen across different bank portals, increasing the risk of unauthorized transactions.

- Increasing number of banks: When a company uses multiple banks for varied services—like local payroll, international trade finance, or treasury—connecting all these threads into a single platform is vital. Otherwise, cash management is likely to be suboptimal and the risk of cash shortages or poor decision-making increased.

- Reporting requirements and audits: For companies in regulated industries, or those that need to report financial results to investors or creditors, the ability to generate consolidated, accurate financial reports is crucial.

Key drawbacks of poor bank-ERP synchronization

Juggling payment files and bank statements manually results in several challenges which, though manageable on a small scale, can quickly multiply as a business grows.

- Time-consuming processes and human error: Relying on file uploads and downloads or manual data entry is error-prone. The risk of duplicate entries, wrong payment amounts, or missed transactions grows exponentially alongside transaction volume. Additionally, finance teams often waste hours consolidating statements from various bank portals.

- Delayed financial insights: If bank statements and payment data are only updated periodically, the ERP system lags behind actual cash movements. Decision-makers may base cash flow forecasts or investment decisions on outdated figures. Especially for multi-entity operations, this can lead to suboptimal budgeting or missed revenue opportunities.

- Reduced scalability: Manual processes quickly hit a ceiling when transaction volumes escalate. Hiring more finance staff to manage integrations manually may work temporarily, but it’s costly and lacks the robust controls that automated systems provide.

- Inconsistent security and compliance: With manual processes, security policies can vary across teams or subsidiaries. Files might be shared in insecure ways (e.g., emai l attachments), increasing the risk of data breaches or fraud. Also, audits become harder because data trails are scattered.

- Fragmented approval workflows: Without integration, payment approvals may happen across different bank portals or email chains. Centralizing payment approvals and reconciliation through an ERP drastically reduces the risk of unauthorized transactions and simplifies auditing.

Three common approaches to bank-ERP connectivity

As detailed in our guide to treasury tooling, ERPs aren’t designed around bank connectivity—they’re broad, all-in-one platforms meant to manage a variety of tasks. Some ERPs may offer off-the-shelf connections to select banks, but generally they lack basic functionality, such as full payment reference details or real-time data feeds, and require significant configuration work.

Similarly, some banks may offer connectivity solutions for major ERP systems, usually relying on batch data exchanges. However, these solutions are typically bank- and country-specific, making them unsuitable for businesses with more than one bank and operations in multiple countries.

In other words, banks and ERPs support integrations with one another, but are not specialized in it. When manual processes become unmanageable, most teams turn to dedicated connectivity solutions.

Manual file transfers or data entry

Manual file transfers and direct data entry may be adequate solutions for small companies, especially when transaction volumes and the complexity of banking relationships are low. With a handful of payments or invoices each week and only one bank being used for day-to-day operations, an investment in a more sophisticated integration might not yet pay off.

Once payment runs grow to hundreds or thousands per month, file downloads and uploads become a bottleneck. Having to log in to multiple portals, handle different file formats, and deal with conversions manually amplifies the chance of error and delays reporting cycles. Plus, with payment approvals and security protocols spread across multiple systems, the risk of policy breaches and fraud is increased.

How it works

At a high level, this process involves logging into your online banking portal, downloading statement or payment files, and uploading them into your ERP. Outgoing payments, such as AP payments, are also exported from the ERP and uploaded to the bank’s portal manually.

Most ERPs include basic tools for uploading payment files or importing bank statements. However, not all bank and ERP file formats are compatible, and these tools may not support automatic format conversion. In these cases, manual data entry may be required.

- Logging into bank portals: The finance team logs into the company’s online banking portals and manually downloads bank statements—often in CSV, Excel, or PDF formats—every day, week, or month, depending on the frequency of transactions.

- Importing statements into the ERP: The files are then imported into the ERP system. This might be a simple drag-and-drop workflow, while other ERPs might require following a specific procedure to match fields like transaction date, reference, and amounts.

- Manual data entry: If the ERP can’t read the downloaded file formats, or if the bank doesn’t provide a suitable export option, users might need to key in transaction details one by one—which can be time-consuming and prone to human error if the transaction count is non-trivial.

- Reconciliation: After importing or entering data, the finance team reconciles each transaction in the ERP’s accounting module. They match incoming cash to customer invoices and outgoing cash to vendor bills or payroll. Any discrepancies—like an unknown transaction—are investigated.

- Uploading payment files back to the bank: When making payments, the ERP typically generates a batch payment file that must be uploaded in the bank portal. Alternatively, payments may have to be entered directly into the bank portal if no export-import functionality exists.

Advantages

- Low upfront cost: Straightforward to get started, requiring minimal technical skill and upfront investment.

- Simple oversight: With low volumes, every payment file or statement can be reviewed before transferral to ensure accuracy, helping keep risk in check.

Disadvantages

- Highly manual: Time-intensive and prone to human error.

- No real-time visibility: All data is only as current as the last upload; if file transfers happen on a periodic basis, such as at the end of every week or month, data may be days or weeks old.

- Future bottlenecks: Doesn’t scale well; manual tasks multiply if you have multiple banks or operate in several currencies.

- Impact on other processes: Adjacent operations such as reporting, cash management, and forecasting must also be handled manually or using separate systems.

Typical use case

Smaller businesses or early-stage companies with low transaction volumes, where automation cost outweighs potential time savings, at least initially.

Building bank-ERP connectivity in-house

Building your own bank-ERP connectivity—or hiring external consultants to do so—might seem like a straightforward choice if you want full control or have highly specific requirements. However, for most companies without extensive in-house IT resources or the appetite for ongoing maintenance, this approach can be costly and lead to future scaling issues.

How it works

This approach involves developing custom integrations to connect your ERP system to one or more banks, requiring specialized IT staff or consultants familiar with a range of bank protocols—SFTP, ISO 20022 XML, and various APIs, for instance. The cost of drafting specifications, coding, testing, and deployment can mount quickly.

Banks also frequently update their API endpoints, file formats (ISO 20022 version changes, for example), and security measures. Each change necessitates code updates, testing, and potential consultant fees. If your business expands to new countries or you add new banking providers, you will likely need to build more integrations from scratch.

Once completed, an in-house bank-ERP integration will likely only automate statement uploads and payment file transfers. Reporting, forecasting, and other cash management activities will remain manual unless you invest further in building those tools.

Advantages

- Full control: The integration can be tailored to specific workflows and data formats.

- No subscription fees: Avoiding payments to an external provider can be beneficial in the short term—though in-house builds often incur larger, unpredictable costs over time.

Disadvantages

- High setup and maintenance overhead: Bank protocols, security requirements, and file formats regularly change, so you’ll need dedicated IT staff or consultants on an ongoing basis.

- Complexity in handling multi-bank connectivity: Each bank may have different protocols, file types, and authentication methods.

- Slower implementation: Building from scratch requires substantial coding, testing, and revision cycles.

- Lack of scalability: In-house solutions necessitate future IT projects in order to support business growth, acquisitions, new banking partners, and regulatory changes.

Typical use case

Large enterprises with significant IT budgets, skilled in-house teams, and in need of highly specialized processes, such as complex approval workflows and custom reconciliation rules.

Using a bank-ERP connectivity solution like Atlar

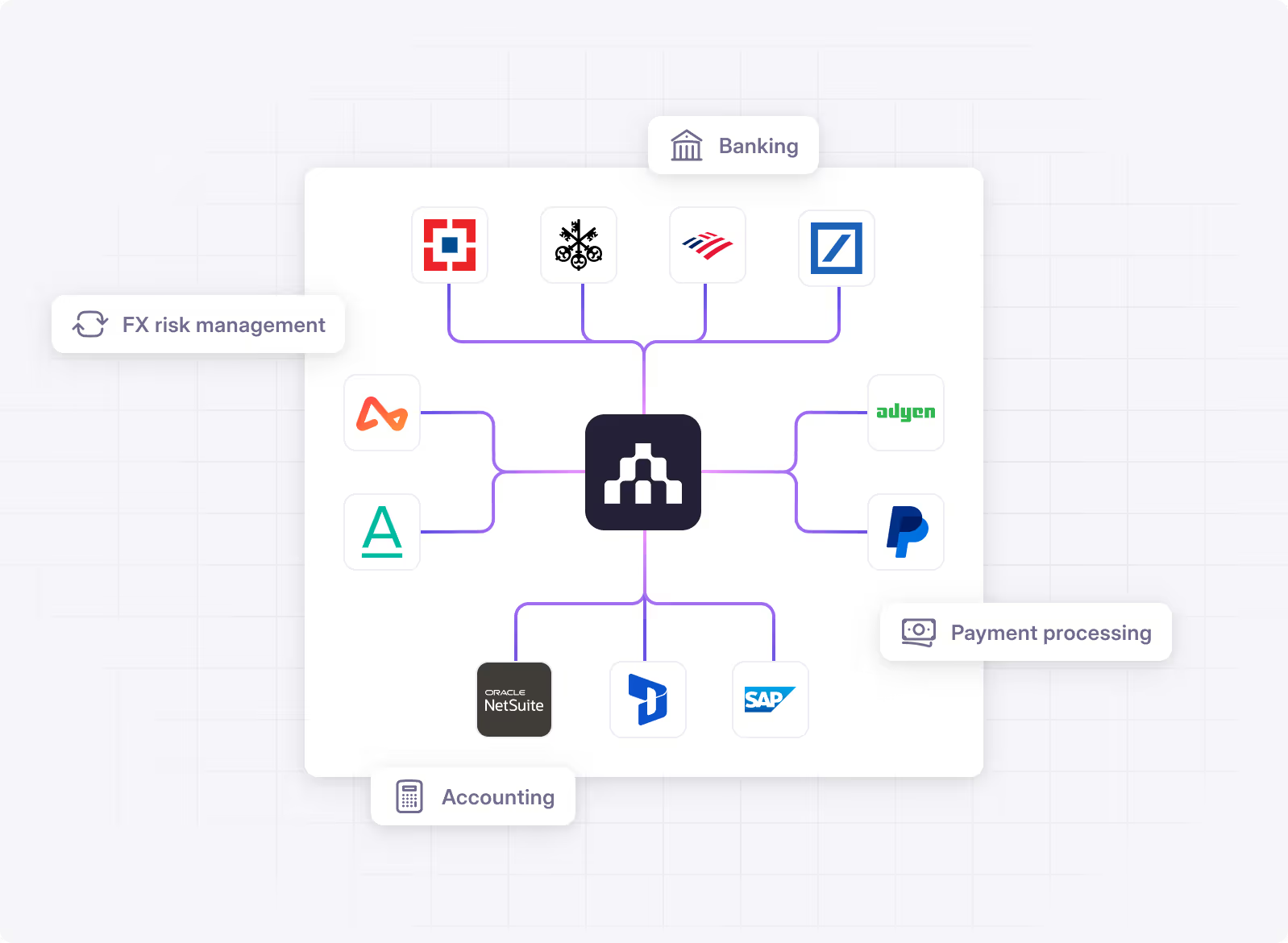

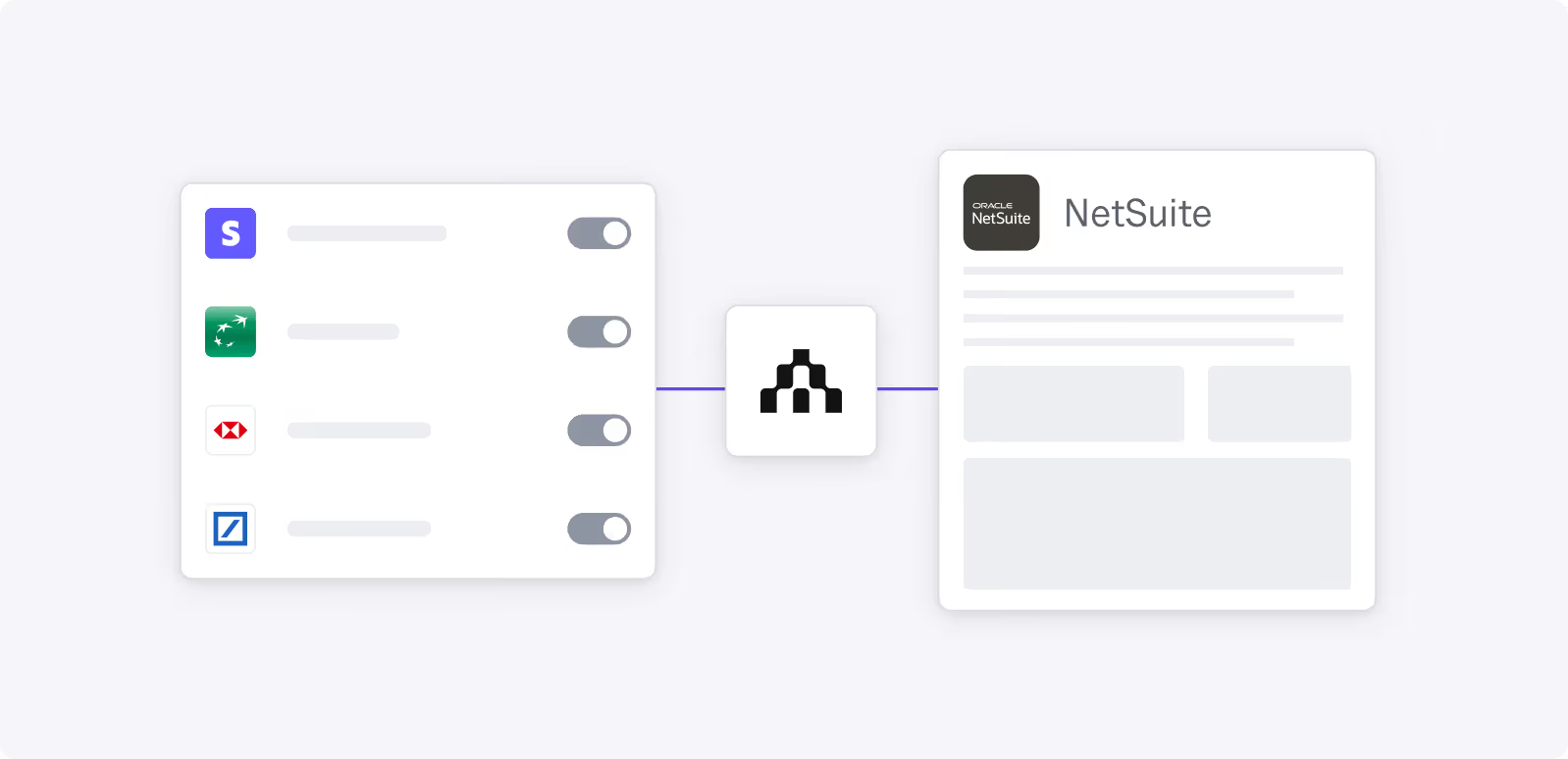

A specialized and fully managed solution such as Atlar takes the complexity of bank-ERP connectivity off your plate, allowing your team to focus on strategic tasks rather than infrastructure. These solutions offer multi-bank connectivity that facilitates an integration between your ERP and any (or many) of your banks.

Atlar, for instance, integrates with Oracle NetSuite, Microsoft Dynamics 365, and SAP S/4HANA—and connects to over 60 major banks as well as payment providers and other finance tools. By using pre-established connections and a proven implementation process, Atlar enables most customers to go live in under 90 days without requiring any IT resources.

How it works

Sometimes referred to as multi-bank connectivity platforms, these solutions offer pre-built integrations with various ERP systems and maintain connectors with several banks. A core part of this offering is a fully managed infrastructure to handle all the technical standards, convert file formats, and adapt to changing security requirements. This means customers don’t need to devote internal resources to maintaining connections or adding new ones.

By design, multi-bank platforms like Atlar support various bank protocols (APIs, SFTP, host-to-host) and file formats (ISO 20022, SWIFT MT940, CSV). Additionally, they handle regular updates and certification cycles, such as the provision of new security certificates and API changes.

Advantages

- Full end-to-end automation: Specialized solutions enable fully automated statement feeds and payment file processing without any manual intervention.

- Faster time to market: Implementation can be up and running quickly; platforms like Atlar offer pre-built integrations and manage the entire onboarding process.

- Multi-bank ready: Platforms typically support various bank protocols and file formats.

- Reduced maintenance: Regular updates and certification cycles are handled by the solution provider, not your internal IT team.

- Lower total cost of ownership: While there’s a service fee, it often compares favorably to the ongoing expense of in-house maintenance or external consultants.

- Benefits beyond bank-ERP connectivity: Platforms like Atlar provide additional features for cash management, payments, and forecasting that can be easily added as business needs change.

Disadvantages

- Subscription fees: Recurring fees are charged for maintenance and feature development.

- Provider lock-in: Reliance on a vendor’s roadmap and uptime makes it important to choose a provider that can support your business now and in the future.

Typical use case

Established mid-market companies and fast-growing scale-ups that are looking for best-of-breed solutions that can scale as they add more banks or payment channels. These companies typically want to offload technical complexity and focus on core finance activities.

Key IT challenges relating to bank connectivity

As most companies with firsthand experience know, bank connectivity projects often turn out to be far more challenging than IT departments realize when they begin. Below are the most common obstacles they encounter along the way.

Data flows and file formats

Multi-bank operations can turn file formatting into a challenge: each bank might have its own implementation guidelines for ISO 20022 or CSV schemas. Managing these differences is critical to ensuring your payments don’t fail or get delayed.

Incoming bank data

- File-based: Banks generate statement files (e.g., CAMT.053, MT940) which are placed in a secure server or transmitted via SFTP. A bank-ERP connectivity solution must be able to pick these up and convert them into a format that’s compatible with the ERP system.

- API-based: For real-time connections, some banks offer REST or SOAP APIs. These APIs may be poorly documented and will need to be monitored for any changes that require updates.

Outgoing payment files or instructions

- File-based: Your ERP’s payment files may need to be converted to a bank-accepted format, such as ISO 20022 pain.001, before they can be transferred. By default, most ERPs support batch payments only—individual payments will require manual processing in the bank’s online portal.

- Direct APIs: A more modern approach is to push payment orders to the bank’s API, which requires a stable and reliable API integration that is maintained on an ongoing basis.

Security and compliance

When dealing with large volumes of sensitive financial and transactional data, security and compliance protocols are key. For bank-ERP connectivity solutions, these measures are fundamental requirements.

- Encryption and authentication: Whether it’s SFTP, FTPS, or an API, data in transit must be encrypted. Banks may require two-factor authentication, IP whitelisting, or mutual TLS.

- Certificate management: Regularly updating SSL certificates and encryption keys is a must to avoid connectivity disruptions.

- Audit trails and logging: A robust setup logs every file or API call. Having a clear record of who initiated payments or changed settings is key for both internal audits and regulatory compliance.

Error handling and monitoring

- Common errors: Connection timeouts, file format mismatches, and mismatched credentials or certificates are typical.

- Monitoring and alerts: Automated systems will send alerts (via email, Slack, or dashboards) if a statement download or file upload fails. This helps teams to fix issues before they escalate.

- Retry logic: Particularly for API-based connectivity, having a built-in retry approach is essential to handle transient network hiccups.

Common pitfalls and how to avoid them

Underestimating maintenance

Whether you go in-house or use a third-party solution, banks update their security protocols, file formats, and APIs with surprising frequency. Regular updates are mandatory and must be managed in a scalable manner.

Ignoring global requirements

If you have international operations, you’ll face multiple bank platforms, local payment schemes, and country-specific compliance rules (e.g., SEPA in Europe). Plan integrations with these variations in mind.

Not having real-time visibility

Manual processes or once-a-day batch uploads prevent you from accessing real-time cash positions. A lack of real-time visibility can lead to suboptimal cash management—if your business is large enough to require multi-bank connectivity, real-time or near-real-time data becomes crucial.

Security gaps

Focusing on connectivity without robust encryption or key management can lead to serious vulnerabilities. In any bank-ERP connectivity solution, data security must be integral, not an afterthought.

How Atlar simplifies bank-ERP connectivity

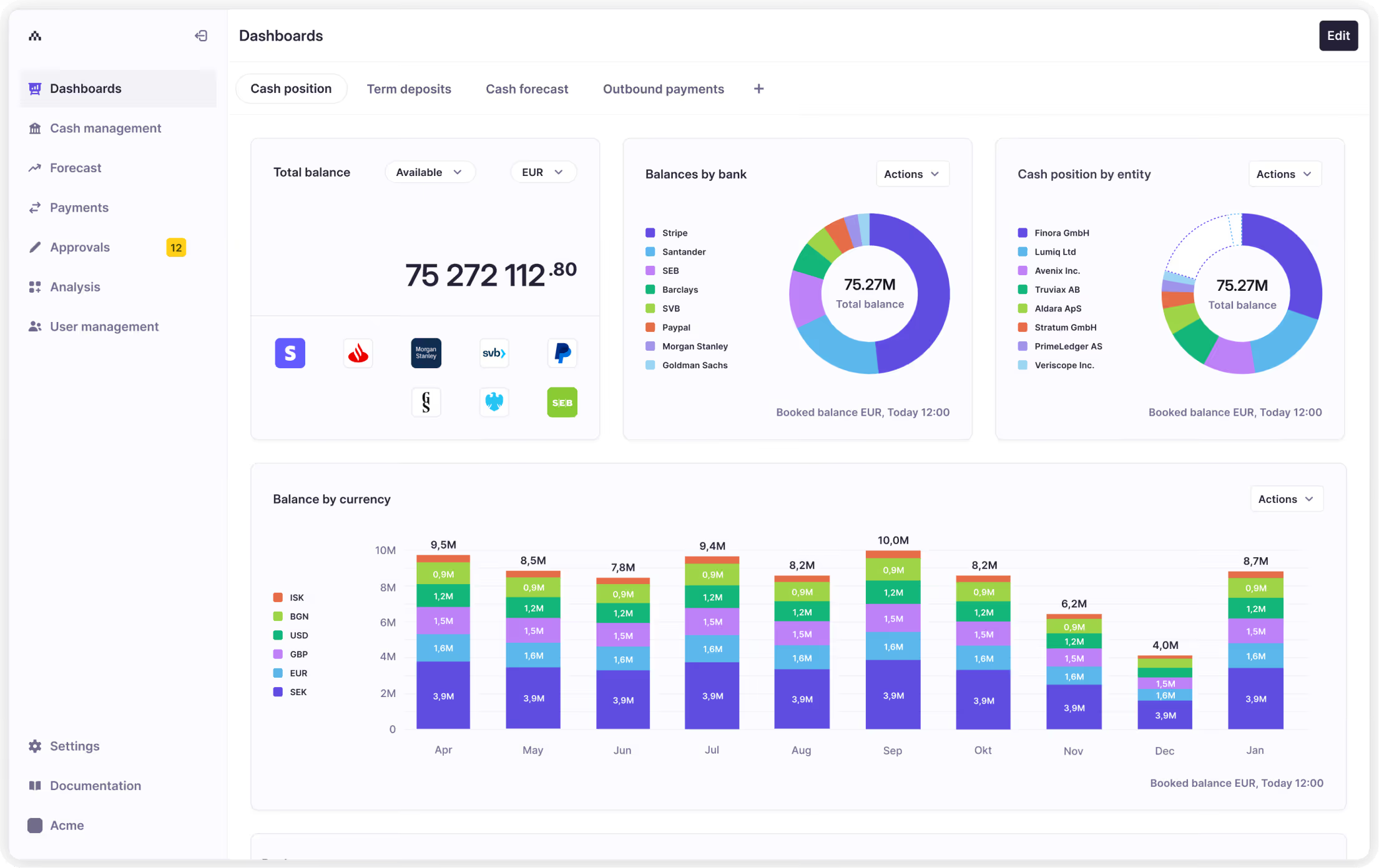

Effective bank-ERP connectivity isn’t just about automation for its own sake. By feeding bank statements into your ERP in real time and securely transferring payment files back to your banks, companies unlock several benefits that make a real difference to the finance team’s effectiveness.

Your day-to-day cash management becomes more efficient, error-prone reconciliation and reporting processes are minimized, and ultimately the business can scale faster by adding new banking relationships and processing higher volumes in a secure, compliant manner.

If your business works with multiple banks and is facing increasing connectivity challenges, it’s worth considering the three main approaches:

- Manual aggregation: Fine for small businesses or those with very light transaction volumes, but it quickly hits its limits.

- Building in-house: Offers total control but demands extensive resources and ongoing maintenance. You’ll need to manage different bank protocols, file formats, and security updates.

- Connectivity solutions like Atlar: Balances automation and simplicity. The investment pays off in saved time and fewer connectivity headaches—especially when dealing with multiple banks and countries.

At Atlar, we help growing companies across Europe—including customers such as Aiven, Zilch, Upvest, Liberis, and more—to remove complexity around bank and ERP connectivity. Our platform connects to multiple banks and ERPs, letting your finance team focus on what they do best—managing finances—not wrangling integrations.

If you’re interested in talking to one of our connectivity experts about your specific use case, don’t hesitate to get in touch.

You can unsubscribe anytime.

Most recent

See Atlar in action.

Enter your work email to watch a live product demo.