Market Deep-Dive: How to Choose the Right Treasury Management System

Introduction

The first Treasury Management System (TMS) was introduced in the mid-1980s as a standalone machine—literally sitting in the corner of the treasury department. Nearly four decades later, demand for treasury software is rising again. One study estimates the market is growing by 14% year over year.

Several factors are driving this growth:

- Increasing financial complexity: As financial markets, regulations, and multi-currency operations become harder to manage, companies seek dedicated treasury tools.

- Macroeconomic pressures: High inflation, low yields, and restricted financing options have made maximizing working capital a top priority.

- The rise of modern SaaS platforms: New entrants like Atlar are making treasury software more accessible and user-friendly, growing faster than legacy TMS solutions.

As a result, more businesses than ever are exploring treasury software for the first time or reevaluating their existing tools. It’s a high-stakes decision—a TMS can be the core of the finance stack, but it can also become a costly, rigid system that’s difficult to maintain or replace.

A previous post compared different options for treasury tooling, from Excel to ERP systems and modern platforms like Atlar. This post takes a closer look at one of those options: the Treasury Management System (TMS).

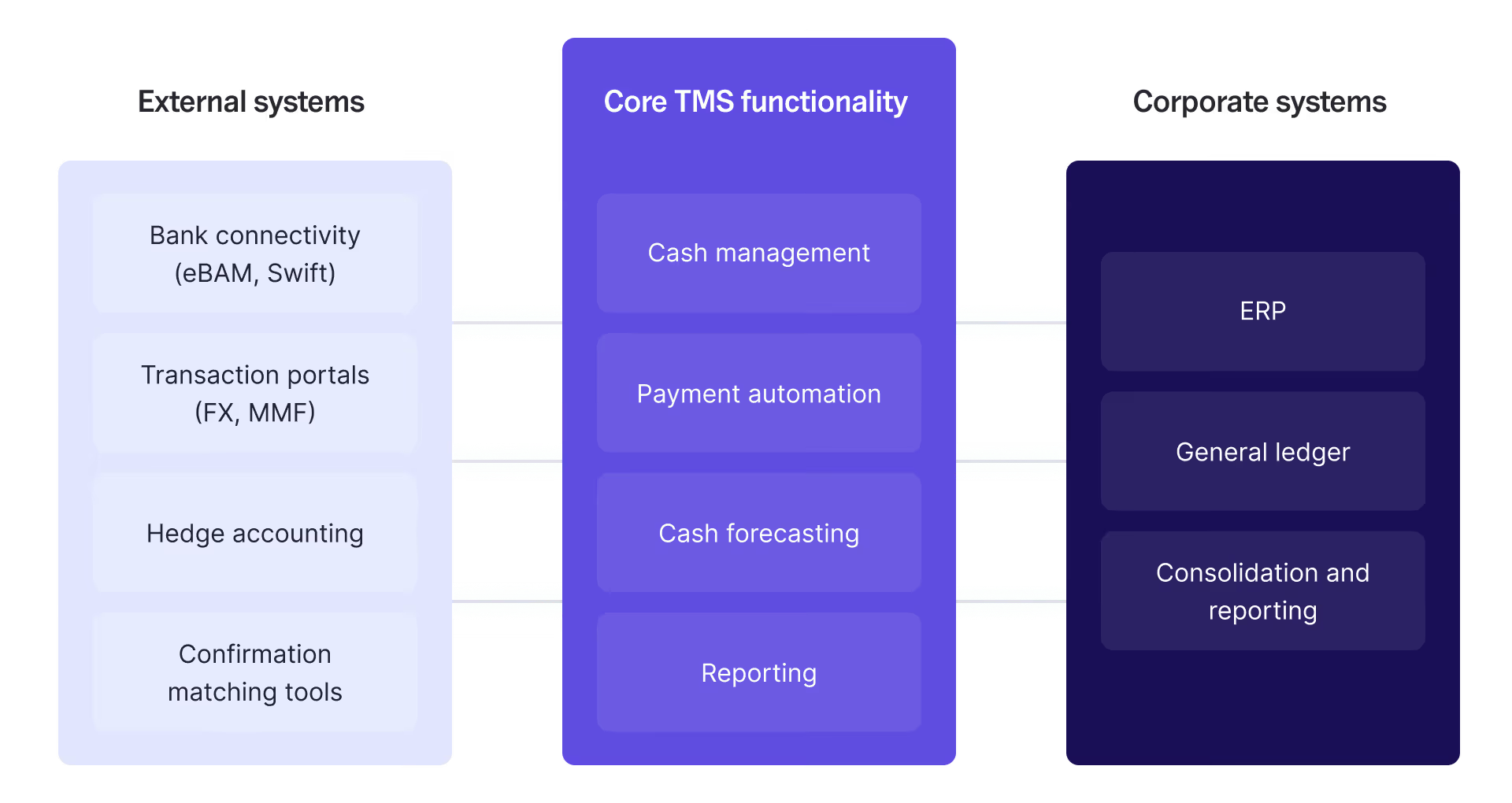

What is a treasury management system?

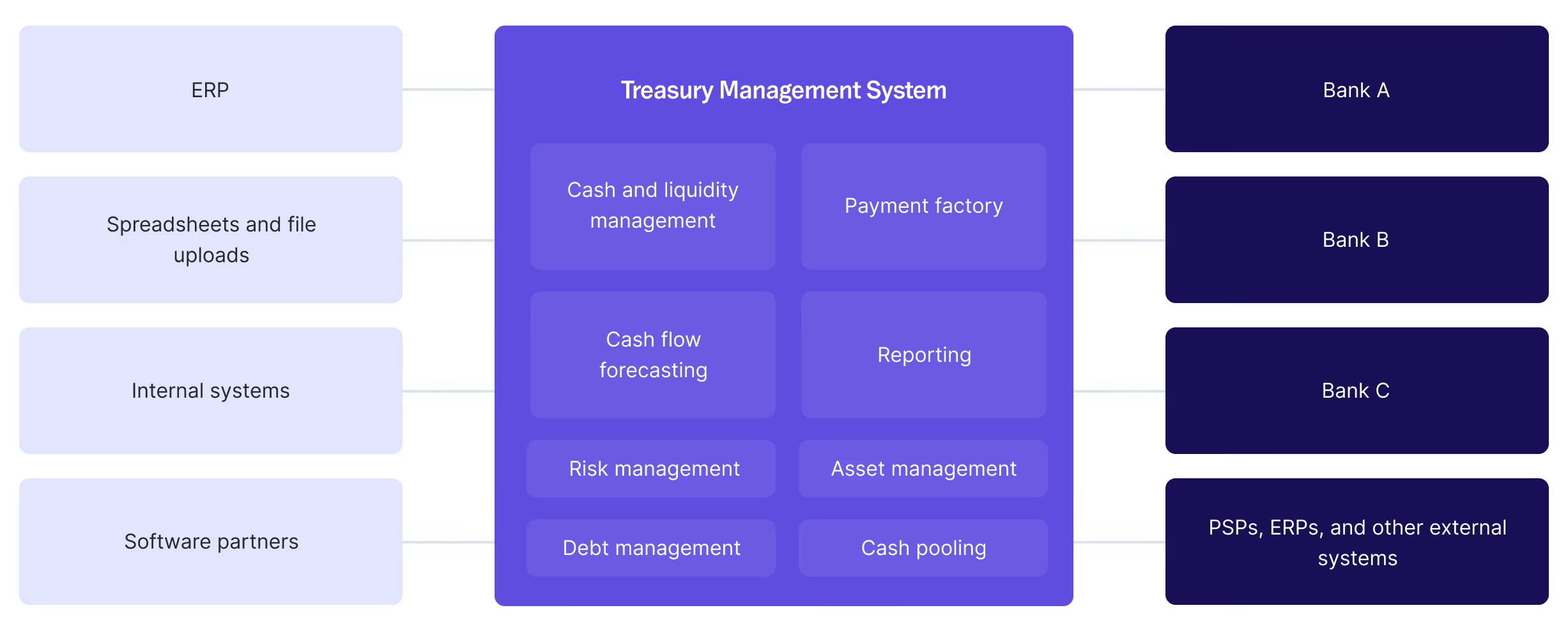

For many large enterprises, a Treasury Management System (TMS) serves as the central hub of their treasury operations, connecting external systems like banks and ERPs with internal finance workflows.

A TMS works by aggregating financial data from multiple sources, standardizing it, and enabling treasury teams to take action based on real-time insights. Key data points include:

- Account balances across all banking relationships

- Financial transactions and historical records

- Expected cash flows across business entities

By consolidating this information, a TMS simplifies reporting, cash forecasting, and financial decision-making. Unlike a read-only tool, most TMS platforms also support payment automation and scheduling, making them essential for companies handling high transaction volumes.

For over thirty years, the Treasury Management System (TMS) has been the go-to solution for enterprises managing core treasury activities. Traditionally, TMS functionality is delivered through separate modules, each requiring individual installation and configuration. Due to the high cost and complexity, TMS solutions were historically reserved for large, well-resourced enterprises.

A new wave of cloud-based treasury platforms is changing this dynamic. Like a TMS, these platforms connect to banks and ERPs but also support real-time API integrations with other financial tools and offer faster implementation.

This shift is driven by technological advancements, particularly the adoption of banking APIs and the growth of real-time payments and data availability. Together, these trends represent the biggest transformation in treasury management in over twenty years, reshaping expectations of what a TMS should do.

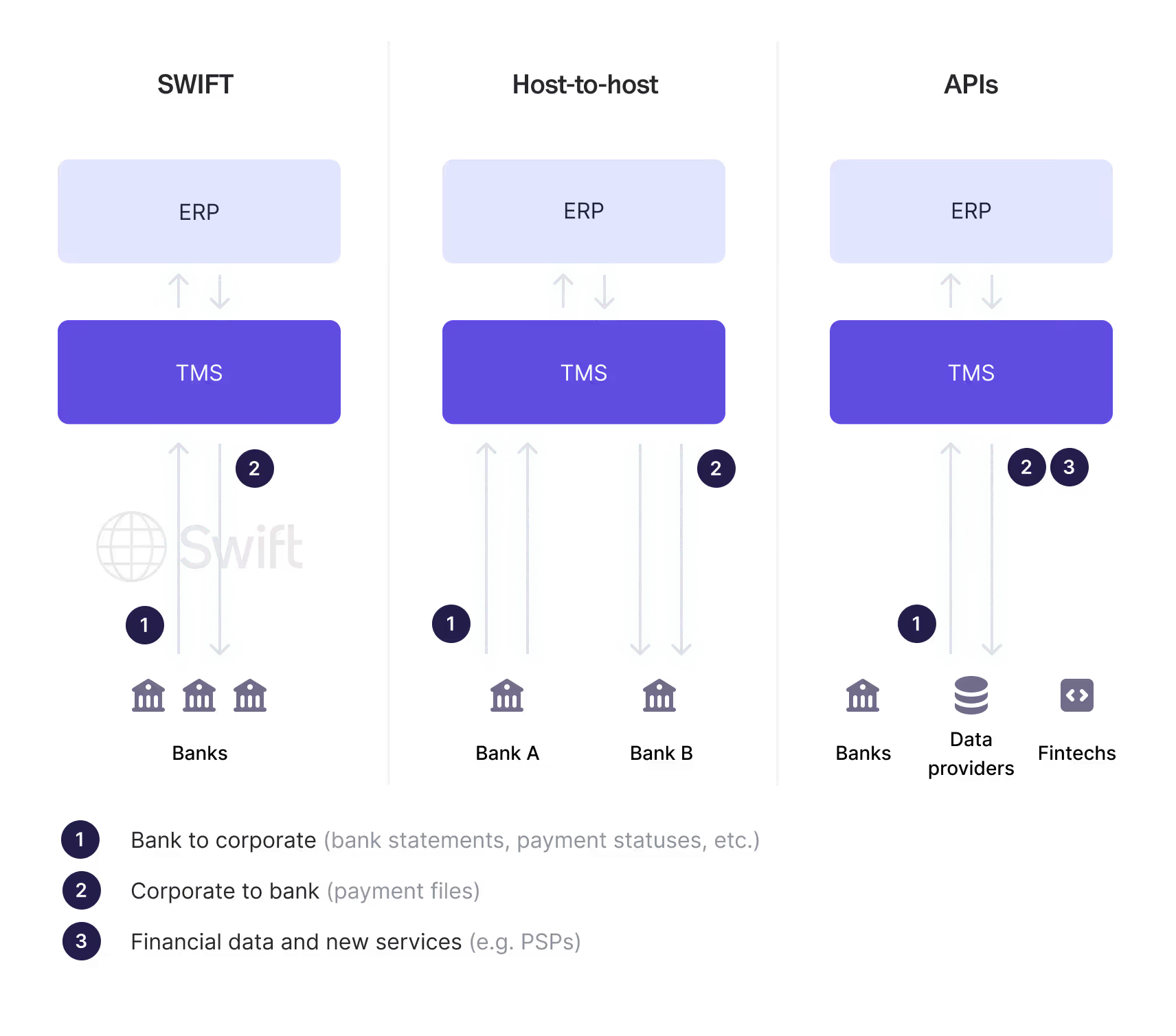

While legacy TMS platforms process data in batches every 24 to 48 hours through traditional channels like host-to-host connections and SWIFT, modern solutions enable real-time data exchange, allowing businesses to access up-to-the-minute financial information from any provider.

What does a TMS actually do?

Here are some of the key functions that a TMS performs:

- Automate manual work: A key benefit of a TMS is the automation of repetitive tasks like transferring data and processing transactions. It helps you track things like exchange rates and payments while simplifying time-consuming processes such as reconciling accounting entries with bank statements.

- Connectivity: The ability to connect directly to banks or other financial institutions through traditional, file-based channels such as host-to-host underpins a lot of TMS functionality.

- Consolidate financial data: TMS software aggregates financial data from banks and other sources, such as an ERP, into one standardized view. This makes it easier to analyze information and simplifies decision-making.

- Liquidity management: Knowing how much cash you have on hand and where it’s located is a basic need of any business. TMS software simplifies cash management by providing a single overview of your liquidity.

- Financial reporting: Most systems come with reporting capabilities that allow companies to generate custom reports for use internally.

- Data security: Protecting sensitive financial data is non-negotiable for most businesses and TMS software includes security features such as encryption, access controls, and audit trails.

- Risk management: A TMS can identify financial risks, such as exposure to interest rate and currency fluctuations, helping businesses to mitigate them and protect their capital.

- Deal management: Some systems, either directly or through third-party services, offer features to manage deals and contracts relating to loans, investments, and FX hedging, and more.

- Multi-currency support: A TMS can typically handle multiple currencies in a way that makes it easier to manage conversion rates and currency risk. This can be a key benefit for businesses with operations in multiple countries.

- Regulatory compliance: For businesses that operate across multiple jurisdictions, a TMS helps in adjusting to new regulations and reduces the risk of noncompliance. Most systems offer approval chains to help enforce internal policies.

Evolution of treasury management systems

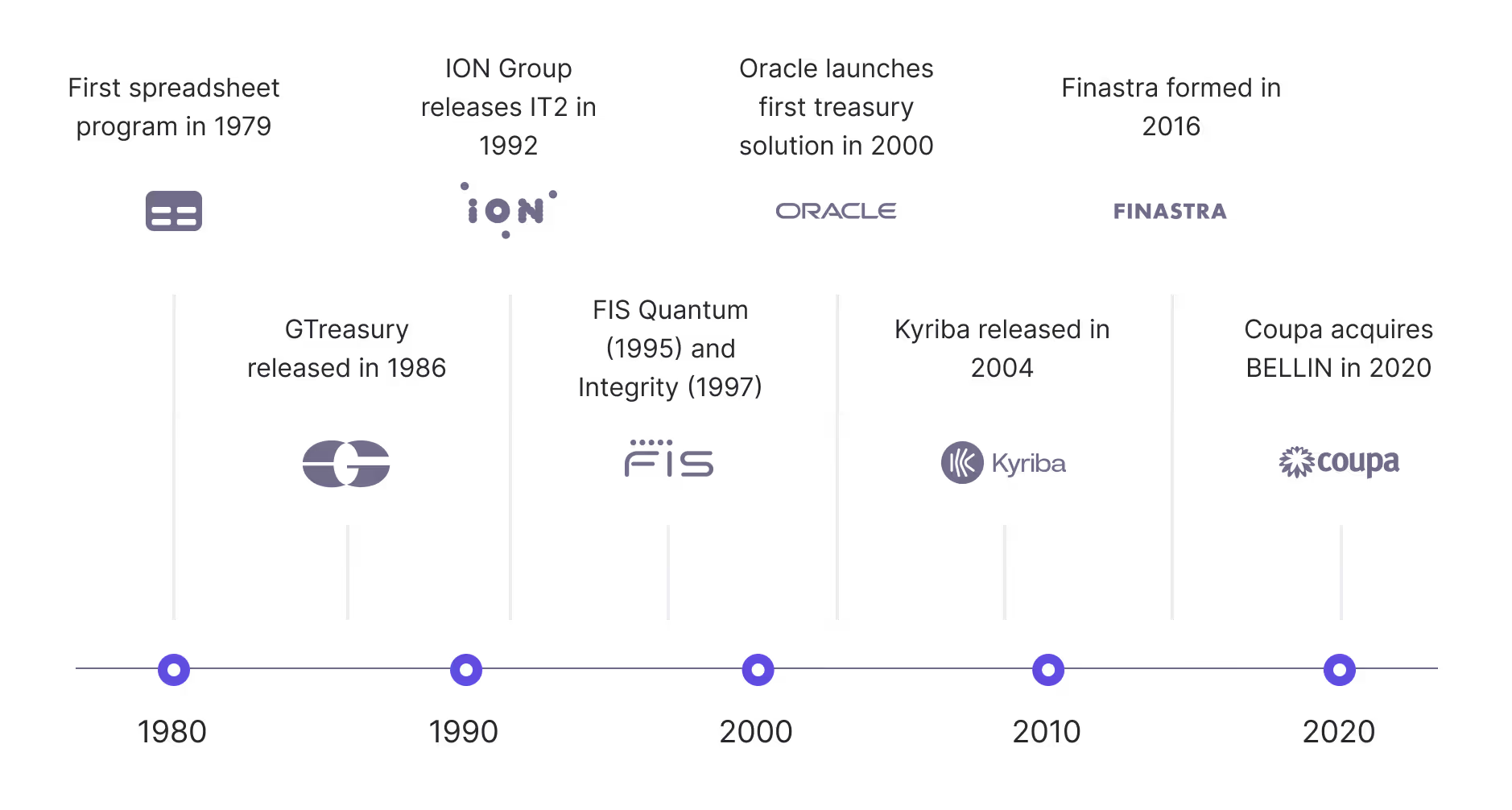

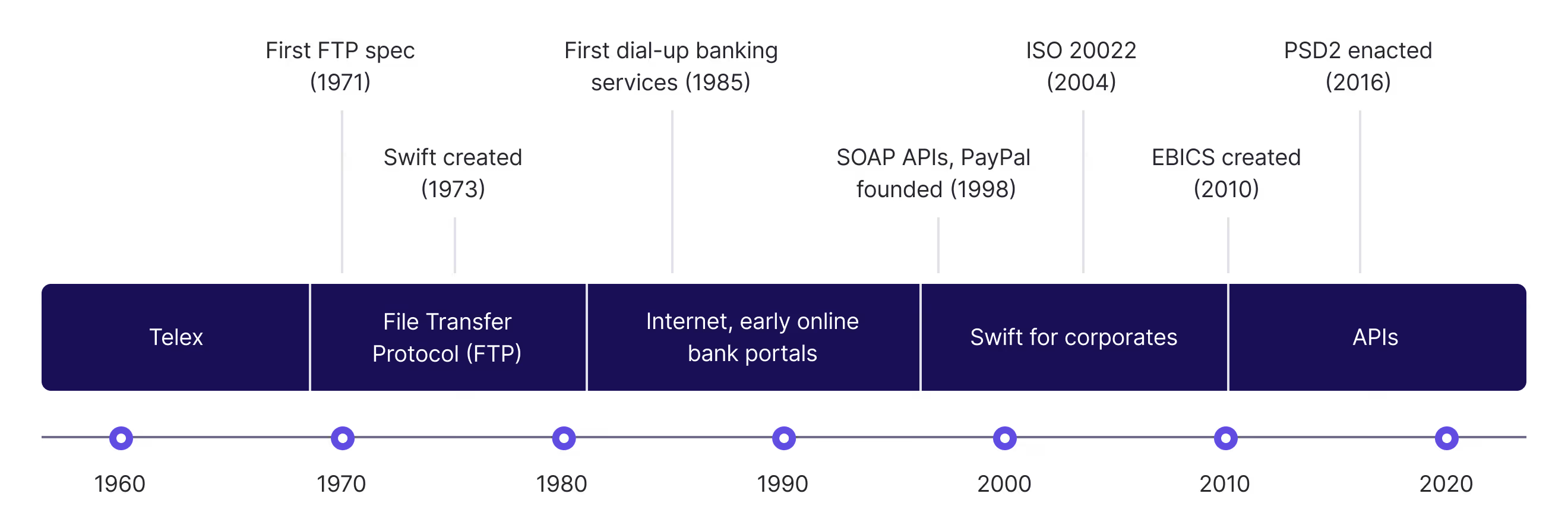

The evolution of Treasury Management System (TMS) software can be divided into two main phases: the first generation of locally installed, self-hosted systems, and the shift to cloud-based platforms in the early 2000s, enabling remote access via web browsers.

The evolution of Treasury Management System (TMS) software can be divided into two main phases: the first generation of locally installed, self-hosted systems, and the shift to cloud-based platforms in the early 2000s, enabling remote access via web browsers.

TMS software first emerged in the 1980s, shortly after spreadsheet programs replaced physical ledgers. These early systems were installed on-premise, allowing businesses to exchange financial data electronically with banks instead of relying on paper documents.

The early 2000s saw the rise of cloud-based TMS solutions, introducing Software as a Service (SaaS) as a new delivery model. While this reduced the effort needed for implementation and maintenance, the underlying technology remained largely unchanged. Crucially, these early cloud-based systems predated APIs, which have since become the primary way software programs communicate.

The gradual adoption of banking APIs paved the way for a major breakthrough: real-time financial data and payments. Today, API-based banking is becoming the norm, and real-time payment networks like Faster Payments (UK), SCT Inst (EU), and FedNow (US) are experiencing rapid growth.

However, most traditional TMS providers—cloud-based or otherwise—have yet to fully embrace these technologies. They still rely on file-based connectivity and batch processing, which Andreessen Horowitz has described as “incredibly antiquated”. While this may not be a dealbreaker for all treasury teams, it does mean that many incumbent TMS platforms provide data that’s a day or two old and struggle to integrate with API-first systems, such as PSPs and modern banks.

Overview of the current treasury software market

Today, treasury teams have an expanding range of technology solutions beyond traditional Treasury Management Systems (TMS). Our guide to treasury management tooling explores these options in more detail.

In addition to ERP treasury modules and bank-provided services, many companies use middleware solutions for niche aggregation services such as electronic bank account management (eBAM) systems and SWIFT or EBICS connectors. Large, well-resourced treasury teams may also choose to build their own in-house system, assemble a "best-of-breed" architecture using multiple specialized tools, or adopt modern treasury platforms, a newer alternative to legacy TMS solutions.

Despite the rise of alternative solutions, the TMS market remains dominated by a small number of global providers. According to Deloitte, the most widely used systems among large enterprises are Kyriba, FIS, ION Group, and SAP Treasury and Risk Management (an S/4HANA module).

TMS solutions have been around for decades—most were introduced between the late 1980s and early 2000s—and today they share several common characteristics:

- Core functionality is largely standardized, with most systems offering cash and liquidity management, cash flow forecasting, and reporting.

- Implementation is lengthy, taking at least six months on average and up to 18–24 months for complex deployments.

- Specialist support is required for implementation, configuration, and ongoing maintenance. Most companies hire external consultants to manage these processes.

- User interfaces are complex, often requiring formal training before teams can use the system effectively. Some providers, like Kyriba, offer paid courses and certifications.

- Updates are infrequent, with most providers releasing major updates only once or twice per year, often resulting in temporary downtime.

- Switching costs are high, making it difficult and expensive to move to another provider. This long-term vendor dependence can lead to less favorable contract terms over time.

How do treasury management systems differ?

While the largest, most complex treasury departments and first-time TMS adopters use similar software for cash management, transaction monitoring, and risk handling, the differences lie in how these systems operate.

The key distinctions between TMS solutions come down to three factors:

- Delivery model: Installed on-premise, hosted privately, or provided as a cloud-based SaaS solution

- Complexity: The depth of functionality and configurability for advanced treasury operations

- Connectivity: The system’s ability to integrate with banks, ERPs, PSPs, and other financial tools

These variables impact cost, implementation time, and long-term business value, making them critical considerations when selecting a treasury system.

Three ways treasury software is delivered

A TMS can be deployed in one of three ways:

- On-premise installation: Installed on a company’s own servers, offering deep configurability but requiring extensive setup and maintenance

- Hosted or managed service: Deployed in a dedicated environment for a single customer, balancing some control with outsourced management

- SaaS (Software-as-a-Service): Fully managed by the provider, requiring no local infrastructure and offering faster deployment

According to a 2022 survey of enterprise-level treasury leads, 42% used a SaaS-based TMS (up from 36% in 2019), while 32% relied on on-premise installations, and 7% used hosted services.

Modern treasury software is increasingly SaaS-based, as it provides a lower-cost, faster-to-implement alternative to legacy systems. While large enterprises often prefer on-premise solutions for maximum configurability and security, these come with higher costs and significantly longer implementations.

Implementation time varies widely based on the chosen system. A 2019 Deloitte report found that traditional TMS implementations take 4 to 18 months, while modern SaaS platforms can be deployed much faster. For example, Atlar customers Sellpywent live within four weeks, and Loomis Pay connected all its bank accounts connected in just three weeks.

Local installation

The traditional delivery method, where the system is installed on company-owned hardware. While offering maximum configurability, it is also the most expensive and time-intensive option.

- High implementation effort: Requires hundreds to over a thousand hours of work from internal IT teams and external consultants.

- Long-term investment: Due to high upfront costs and switching barriers, companies typically commit to a provider for several years.

- Complex user experience: Treasury teams require specialized training before they can effectively use the system.

- Infrequent updates: System upgrades occur once or twice per year, often requiring up to 24 hours of downtime.

Examples of providers offering local installation include FIS (Quantum), ION Group, and SAP.

Hosted service

A hosted service is a single-tenant solution hosted by the provider but dedicated to a specific customer. This allows for some customization while outsourcing infrastructure management.

Providers that offer a hosted service include Coupa, GTreasury, and EcoFinance.

Software as a Service (SaaS)

SaaS platforms are cloud-based solutions accessible via a web browser, eliminating installation and maintenance burdens.

Launched in 2004, Kyriba and Nomentia were two of the earliest cloud-based treasury systems. Broadly speaking, this category also includes the new wave of SaaS platforms such as Atlar itself.

Depth and complexity of functionality

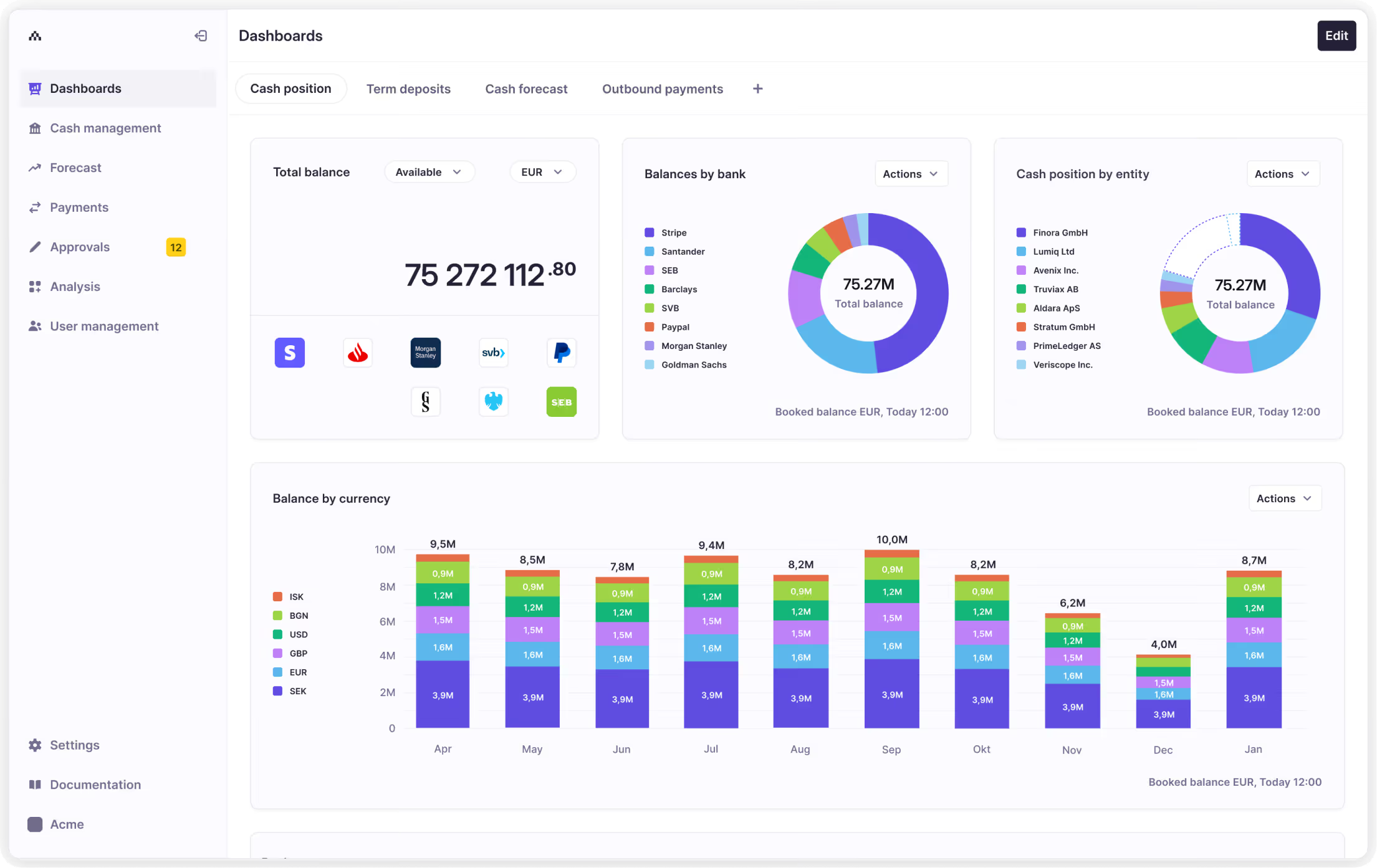

All treasury systems cover core functionalities like cash and liquidity management, forecasting, and reporting. Some, including Atlar, also integrate payment capabilities, often referred to as a "payment factory." This allows for:

- Direct payment processing within the system

- Automated account statement imports

- Centralized management of approvals and counterparties

Beyond core features, more complex TMS solutions cater to larger treasury teams with:

- Risk management (interest rate and currency exposure)

- Investment and debt management

- In-house banking (cash pooling, inter-company loans)

When evaluating a TMS, companies should differentiate between critical and optional features. More functionality isn’t always better—increased configurability raises costs and complexity, slowing adoption if extensive training is required.

Traditional versus API-first connectivity

Connectivity underpins all treasury software. Without bank connectivity, treasury teams lack the necessary cash visibility. Without ERP connectivity, teams find themselves operating in an information silo that lacks the internal financial data needed to plan and forecast.

Historically, bank connectivity was the primary focus of treasury software, relying on batch-based file transfers through well-established channels such as Secure File Transfer Protocol (SFTP) and Swift connections. These connectivity channels use batch-based processing, meaning that data is sent on a predefined schedule every 24 or 48 hours.

Some TMS providers offer more prebuilt bank connections than others, and some have integrated more channels than others. Not all providers support regional channels like Europe’s EBICS, for example. Still, connectivity has not been as a major point of differentiation.

Two recent developments have broadened the scope of treasury connectivity beyond that of the traditional TMS. One is the unbundling of corporate banking services by API-first tools for spend management, procurement, payments, and more. Think Revolut, Adyen, PayPal, Spendesk, and others. These systems, which connect to one another almost exclusively over API, have gone from niche, specialized tools to critical parts of the modern finance stack in just a few years – leading to financial data being spread across multiple systems.

The second trend is the proliferation of real-time payment and data capabilities. Over the last decade, key parts of the payment infrastructure in Europe and the US have been upgraded to support real-time payments. Banks, in turn, have exposed their APIs to make real-time payments available to customers, leading to the exponential growth of several instant payment schemes—now used widely by consumers and increasingly businesses too.

Treasury connectivity in the future is set to revolve around APIs and real-time processing. The ability to manage cash positions on demand, rather than viewing the prior day’s data, is a major advantage. In a Deloitte survey of 245 treasury leads, 86% of respondents had already implemented API connectivity or are considering doing so in the near future.

This shift presents a challenge to the legacy TMS. As of today, many such systems are unable to integrate with API-first platforms or even a traditional bank’s modern API offering. Modern treasury platforms that have emerged over the last five or so years, in the midst of the API revolution, are one alternative. To learn more, read our deep-dive on bank connectivity.

When and why companies invest in treasury software

Companies investing in new treasury software generally fall into one of three categories. Identifying which type best describes your organization can help determine whether a TMS is the right fit:

- Companies without dedicated treasury software

- Companies upgrading as part of a transformation project

- Companies reviewing a long-standing TMS

Investing in treasury software is a strategic decision that depends on a company’s current setup, pain points, and long-term goals. Whether replacing manual processes, upgrading an outdated system, or reviewing an existing solution, businesses should focus on scalability, automation, and integration to maximize long-term value.

Companies without dedicated treasury software

These companies typically rely on manual processes using bank portals, file transfers, and spreadsheets. Their goal is to streamline treasury operations, automating tasks to reduce manual data entry and improve cash visibility. A TMS provides better control, audit trails, and a centralized system for treasury activities.

Common drivers include:

- Establishing a dedicated treasury function for the first time

- Reducing time spent on manual processes

- Replacing fragmented tools with a more integrated solution

Since most TMS solutions meet these needs, ease of implementation, usability, and integrations should be key selection criteria. Treasury systems have traditionally catered to large enterprises, so modern teams may find legacy platforms difficult to adopt without specialized support.

Companies upgrading as part of a treasury transformation

These companies may already use a TMS or a similar solution but find it outdated, inflexible, or poorly integrated with other finance tools. Their main challenges include:

- Disconnected systems: Multiple platforms that don’t communicate, requiring manual file transfers

- Slow processes: Batch-based data updates (e.g., every 24–48 hours) limiting real-time cash management

- High maintenance effort: An aging TMS that requires significant upkeep

A modern treasury platform can unify data, improve efficiency, and enable real-time processes. Companies in this category should ensure core functionality is met while also evaluating next-generation capabilities like API connectivity and real-time data processing to future-proof their treasury operations.

Companies reviewing a long-standing solution

Organizations that have used a TMS or equivalent solution for several years may periodically benchmark their system against newer solutions. This could be triggered by:

- Internal policy reviews

- Corporate events (e.g., mergers or acquisitions introducing new banks and currencies)

- Cost-saving initiatives (e.g., shifting from an on-premise system to a SaaS model)

These treasury teams generally have well-defined requirements, but the challenge is avoiding a check-the-box approach that overlooks long-term adaptability. A heavily customized system may address immediate needs but could struggle to keep pace with new technologies and evolving business demands.

How much does a TMS cost?

Acquiring a TMS is a significant investment. As with any major expenditure, CFOs expect a return on investment (ROI) analysis upfront. However, this can be challenging, as traditional TMS implementations are lengthy and complex, often taking years to demonstrate ROI. Additionally, some benefits are qualitative rather than financial.

The total cost of a TMS includes the initial purchase price, one-time and recurring fees for implementation and data migration, as well as ongoing expenses like maintenance, specialist support, and training. Pricing models vary by provider, but general benchmarks exist:

- Businesses with complex treasury needs, international operations, or multiple entities typically invest over $100,000 per year for a robust TMS.

- Mid-size businesses with simpler needs can expect to pay up to $40,000 per year for a standard, off-the-shelf solution.

- Implementation fees often amount to up to 15% of the annual contract value, excluding additional integrations such as bank-ERP connections, which cost around $5,000 per connection.

- Professional services—including data migration, system configuration, and support—add another 20-25% of the annual contract value.

In total, a well-implemented TMS with some customization and up to three ERP-bank connections may cost around $160,000 in the first year and $140,000 annually thereafter. Over five years, this adds up to approximately $646,000 (adjusted for inflation), according to Financial Sciences, maker of the ATOM TMS. Notably, this estimate excludes transaction-based fees, which some providers charge based on account and transaction volume.

Beyond direct costs, ‘invisible’ expenses such as additional implementation support, customization, and training can add up. Many companies find that specialist consultants are essential during implementation, and teams often require multiple training sessions before using the system effectively.

Given an implementation timeline of 4–18 months, a TMS is a long-term commitment. While the investment may only be justified for organizations with complex treasury needs, companies with clear use cases and sufficient resources can be confident in achieving ROI over time.

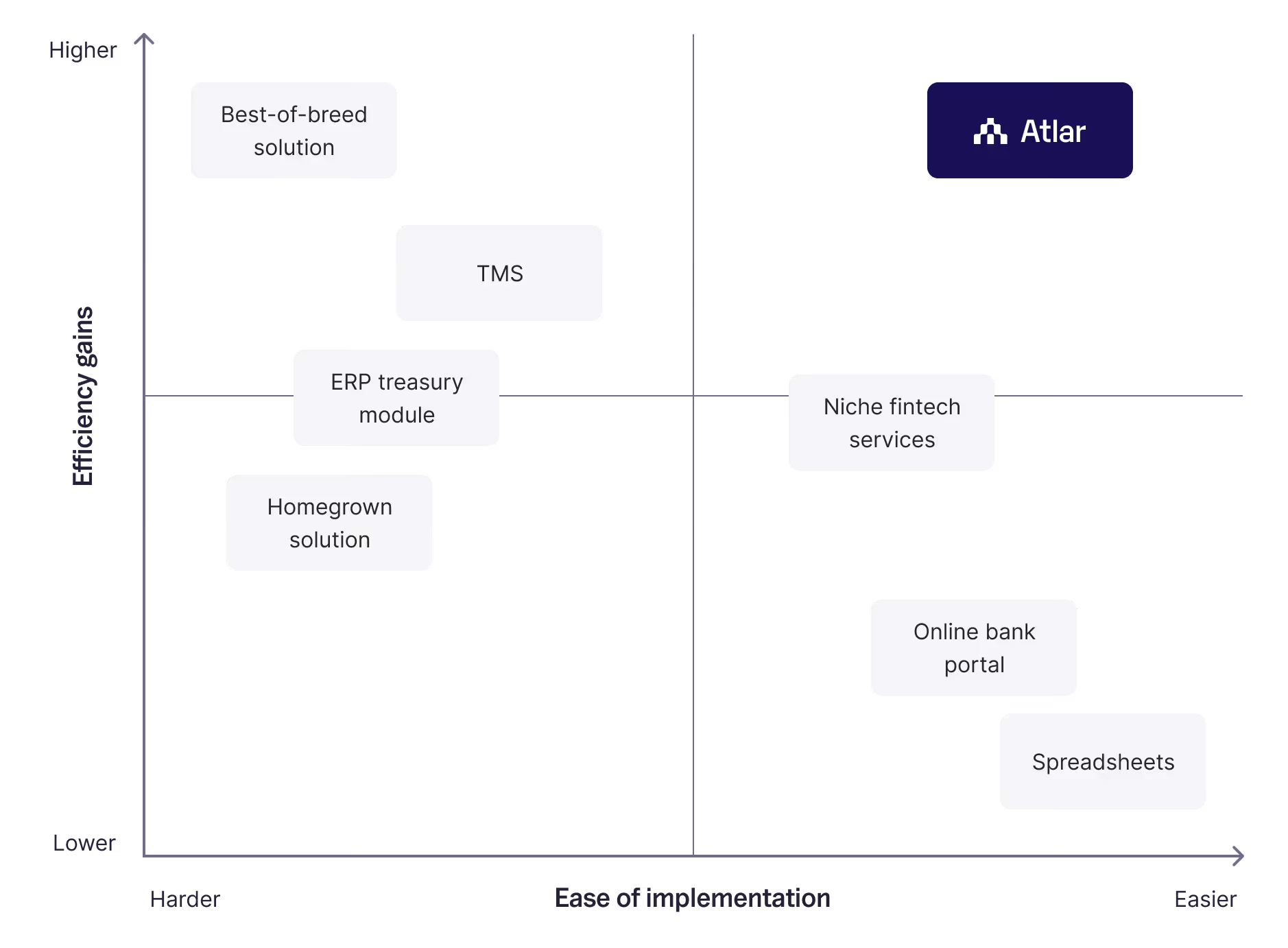

What are the alternatives to a traditional TMS?

Until recently, treasury teams had a binary choice: a complex, high-cost TMS with a long implementation or manual spreadsheets prone to errors and inefficiencies—legacy software or none at all.

Given the cost and effort required to implement a TMS, many companies still rely on spreadsheets for parts of their treasury operations. While spreadsheets are accessible and easy to use, they come with significant drawbacks: they’re error-prone, easily altered or corrupted, and require extensive manual work. Though useful, they are not a scalable long-term solution for a growing treasury team.

A middle ground is emerging with modern treasury platforms that combine the core functionality of a TMS with API connectivity, real-time reporting, and user-friendly tools. These solutions are faster to implement, easier to use, and more cost-effective, making them ideal for businesses managing multiple banks but with limited budgets for IT and treasury tooling.

Implementing treasury software requires upfront investment, but platforms like Atlar significantly shorten the time to ROI, reducing the risks typically associated with new software. While a traditional TMS can take up to 18 months to implement, Atlar is up and running in just 2–3 months. Unlike legacy TMS interfaces, modern treasury platforms prioritize UX and ease of use, making advanced features like forecasting accessible without specialist training.

Built on a SaaS model, modern treasury platforms may not yet offer the deep configurability of on-premise TMS solutions developed over decades. The largest, most complex treasury teams may continue to rely on heavily customized systems. But for most businesses, the best TMS alternative may not be a TMS at all—it’s a faster, more modern solution.

How Atlar can help

Over the past two decades, financial technology for consumers has evolved rapidly—but treasury software has lagged behind. The treasurer’s toolkit is overdue for an upgrade. Atlar is rebuilding it from the ground up with modern, real-time technology, allowing finance teams to level up without years-long implementations, costly consultants, or ongoing maintenance headaches.

Atlar provides customers like Acne Studios, GetYourGuide, and Forto like Acne Studios, GetYourGuide, and Forto with a single platform that connects to all their banks and systems—up and running in weeks. By automating manual tasks and improving cash management, finance teams can focus on what truly matters instead of getting buried in admin work.

Considering a treasury system? Book a demo and see why modern teams choose Atlar.

You can unsubscribe anytime.

Most recent

See Atlar in action.

Enter your work email to watch a live product demo.