The Ultimate Guide to Cash Flow Forecasting

Cash flow is a key concern for businesses of all sizes and stages. Cash management—monitoring and optimizing current cash balances—is essential to meet financial obligations, maintain liquidity, and invest for growth. Equally important is predicting how those balances will change over time as a result of future cash inflows and outflows.

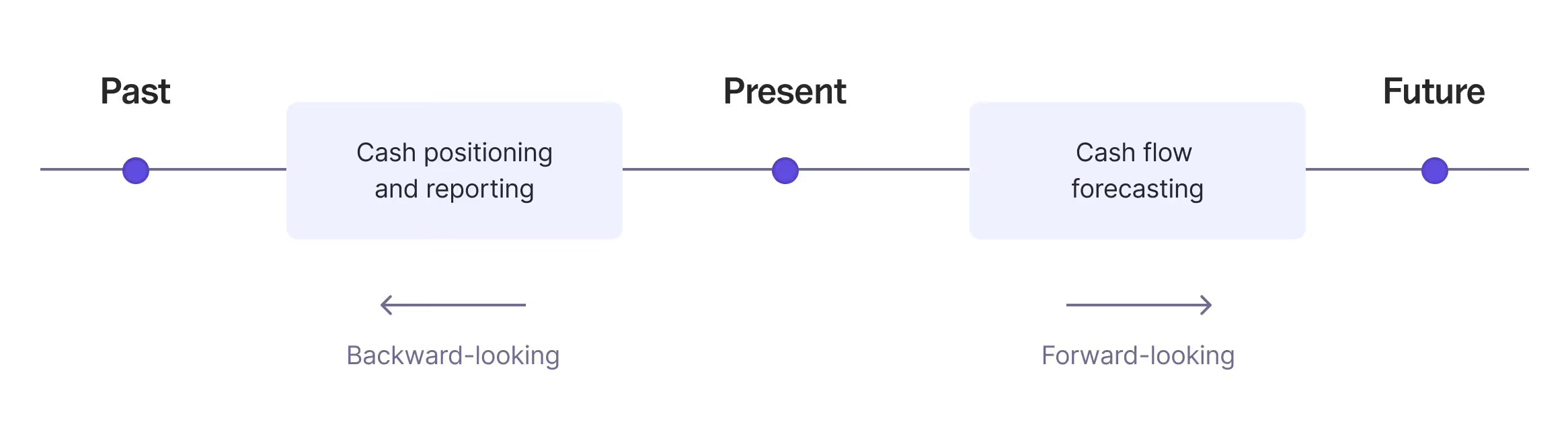

This is where cash flow forecasting comes in: it projects the movement of cash into and out of your business, helping you plan for potential surpluses or shortfalls. While cash positioning shows current cash availability, cash flow forecasting projects the future cash position for the weeks, months, or quarters ahead. Together, they give finance teams a complete view of cash management.

Forecasting serves as the foundation for most short- and mid-term cash and liquidity strategies, enabling companies to efficiently manage accounts payable, debts, investments, and much more. Among various forecasting models, the 13-week cash flow forecast is the most widely used.

This in-depth guide covers the main reasons for adopting a 13-week forecast along with detailed tips on model design, data collection, automation, and software options to support your forecasting process. Atlar helps customers like Aiven, Zilch, and Liberis to automate 13-week forecast creation using real-time bank and ERP data. To learn more, check out our cash flow forecasting solution or see a live demo.

Why companies forecast cash flow

Companies create forecasts generally—such as sales or revenue forecasts—to gain insights into their business and make informed decisions. Companies forecast cash flow specifically to understand the money flowing through the business—its liquidity—and maintain control over it.

Although cash flow forecasting may seem similar to forecasting revenue or profitability, it serves a distinct purpose. While cash flow and profitability are related, they differ in timing: cash flow tracks actual cash movement, whereas profitability includes revenue earned but not yet received (accounts receivable). Both profitable and unprofitable businesses rely on cash flow forecasting to manage their liquidity.

The timing difference between cash flow and profitability can be significant: a company needs cash on hand—not just accounts receivable—to maintain operations and pay employees and suppliers. A study by U.S. Bank (cited here) found that 82% of business failures are due to cash flow issues. Even cash-rich businesses are vulnerable to working capital risks if they expand rapidly with a poor cash conversion cycle (CCC), poorly time outgoing payments, misallocate cash, repay large debts prematurely, or have funds tied up in non-liquid assets.

However, a business with an accurate cash flow forecast can at least anticipate shortfalls and surpluses and plan accordingly. This is why most finance leaders view cash flow forecasting as essential to cash and liquidity risk management—and why management teams increasingly agree, especially given recent market volatility and supply chain disruptions. Here are some of the key drivers for forecasting in more detail.

Predict cash shortfalls

Cash shortfalls can occur for several reasons, such as during months with an additional payroll cycle, periodic tax payments, or when stocking up on inventory ahead of a busy sales season. By anticipating negative cash flow in advance, companies can plan ahead. This may involve delaying payments to suppliers, shortening payment terms for customers, or planning for alternative sources of capital, such as securing financing or selling assets.

Exploit cash surpluses

With a predicted positive cash flow, a company can plan how to use its cash surplus—whether by paying down debt, investing to grow its funds, or reinvesting in the business. An accurate forecast enables companies to allocate funds confidently to maximize returns, such as by moving cash into a high-yield savings account or money market fund (MMF).

Enable day-to-day cash management

By providing visibility into specific inflows and outflows at a per-transaction level, a short-term cash flow forecast like the 13-week model is an important tool for daily cash management operations. It helps finance and treasury teams allocate cash efficiently across operational expenses, optimize payment timing, and ensure that sufficient working capital is available to support business initiatives.

Model and analyze scenarios

By creating different cash flow scenarios—such as optimistic, pessimistic, and baseline forecasts—companies can better understand how factors such as changes in revenue, unexpected expenses, or shifts in payment timing might impact their cash position. This allows companies to prepare for potential risks that may arise under different conditions and evaluate the impact of strategic decisions, such as hiring, expansion, or new projects, on future cash flow.

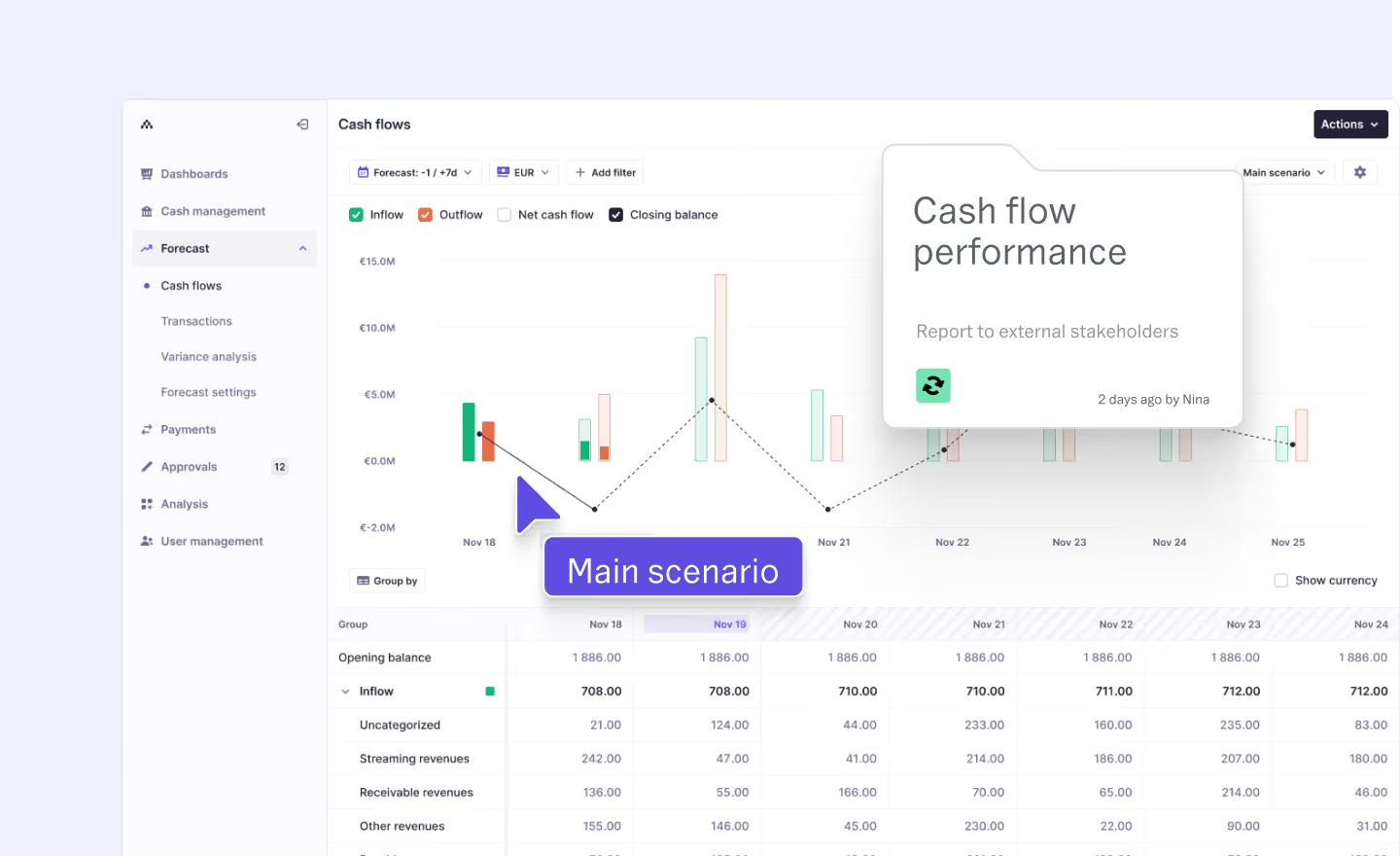

Report to external stakeholders

Several external parties often require cash flow forecasts before transacting with a company. Banks typically request a cash flow forecast because it allows them to assess a company’s ability to service its debts. Investors also review forecasts to understand the company’s cash position and evaluate its efficiency in managing the full cash conversion cycle.

What is the 13-week cash flow forecast?

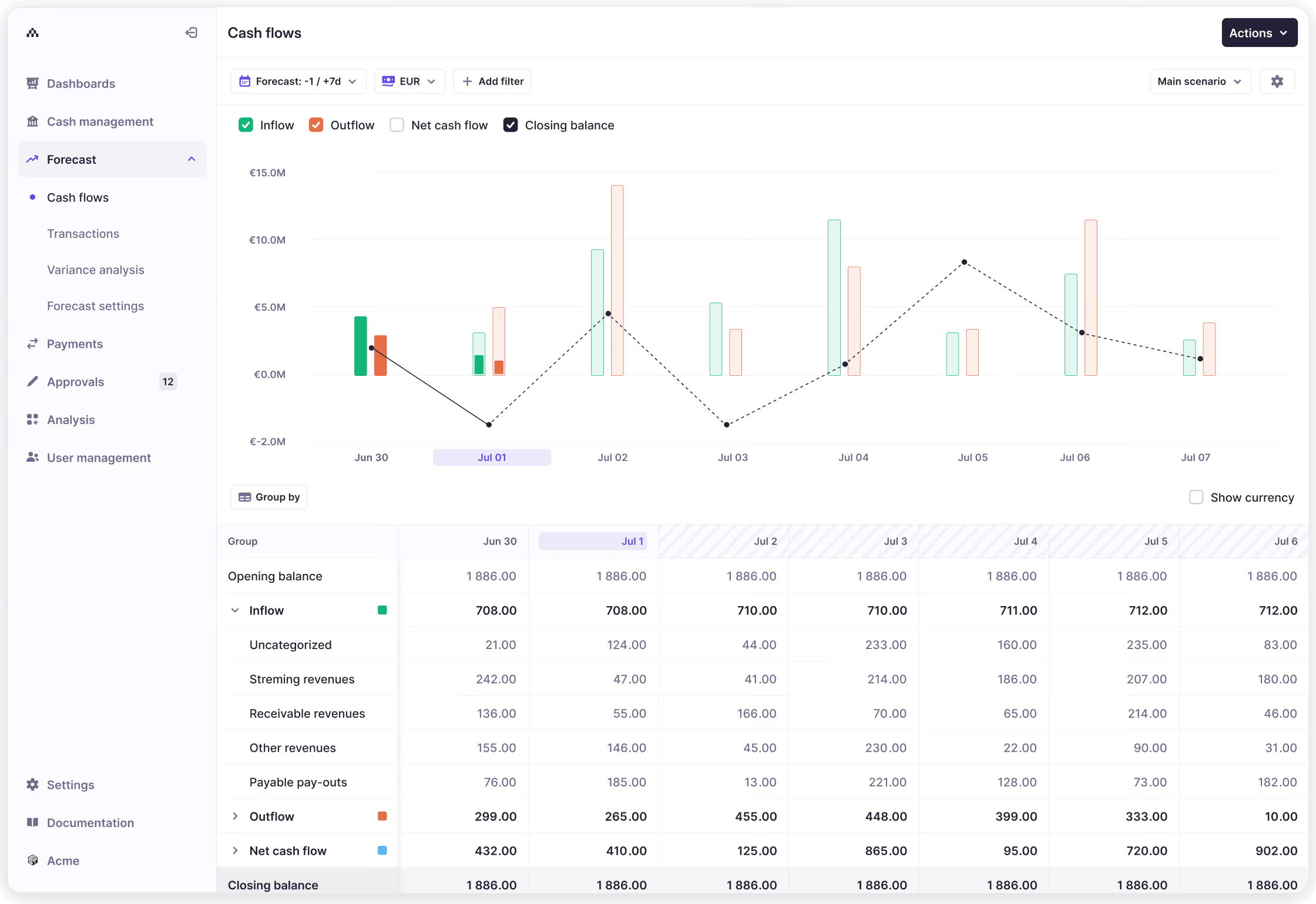

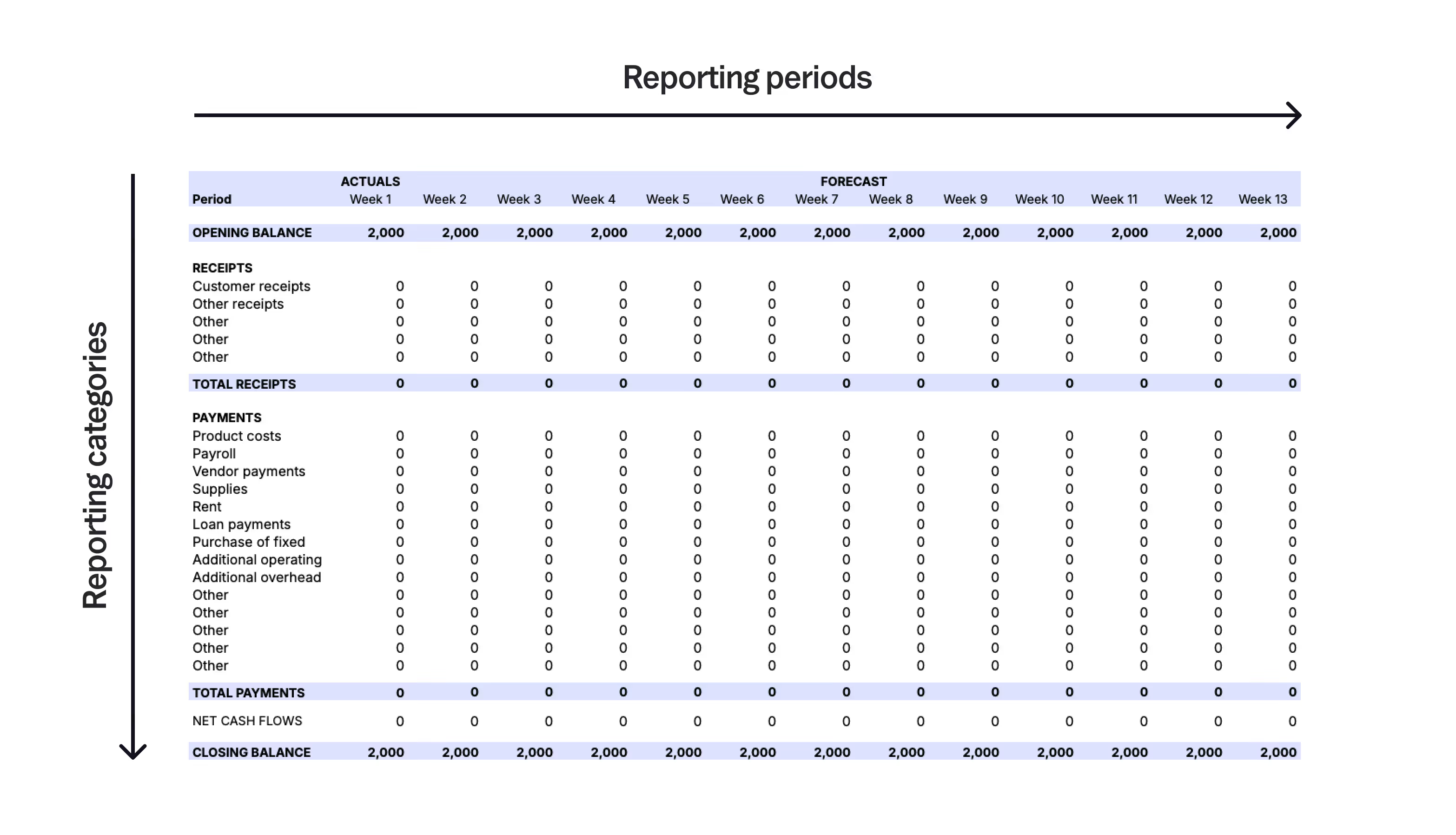

The 13-week cash flow forecast is the most widely used type of short-term forecast. While longer term forecasts project a company’s cash flow over a period of six months to five years, the 13-week forecast focuses on the cash you have, the cash you expect to receive, and the cash you expect to pay out of your business over a 13-week period. Here’s an example of this in the Atlar dashboard, followed by some of the key characteristics of 13-week forecasts generally.

Quarterly time horizon with weekly detail

The 13-week timeframe covers one fiscal quarter, giving you a manageable yet comprehensive view on cash flow that extends to the next key reporting date or quarter-end. Consisting of weekly periods, it also allows for close tracking of specific inflows and outflows—helping to capture payment cycles, seasonal patterns, and other short-term fluctuations in cash.

Direct forecasting method

Most 13-week forecasts use the “direct” forecasting method, tracking actual cash receipts and payments for transactions that have occurred or are expected to occur. This approach provides a real-time view of cash activity, which is crucial for day-to-day liquidity management. By contrast, longer term forecasts often use the “indirect” method, meaning that they rely on indirect adjustments from net income.

For example, a company’s forecasted cash flow statement—often included as part of its quarterly or annual budget or business plan—is derived indirectly from the forecasted income statement and balance sheet. Unlike the 13-week forecast, it’s intended to show the broad categories of where cash is generated and spent over a longer timeframe.

Non-cash items excluded

Another key difference between the 13-week forecast and other, longer term forecasts is that it doesn’t include non-cash accounting items such as depreciation and accruals for various expenses. Rather, it’s designed to precisely capture specific inflows and outflows of cash.

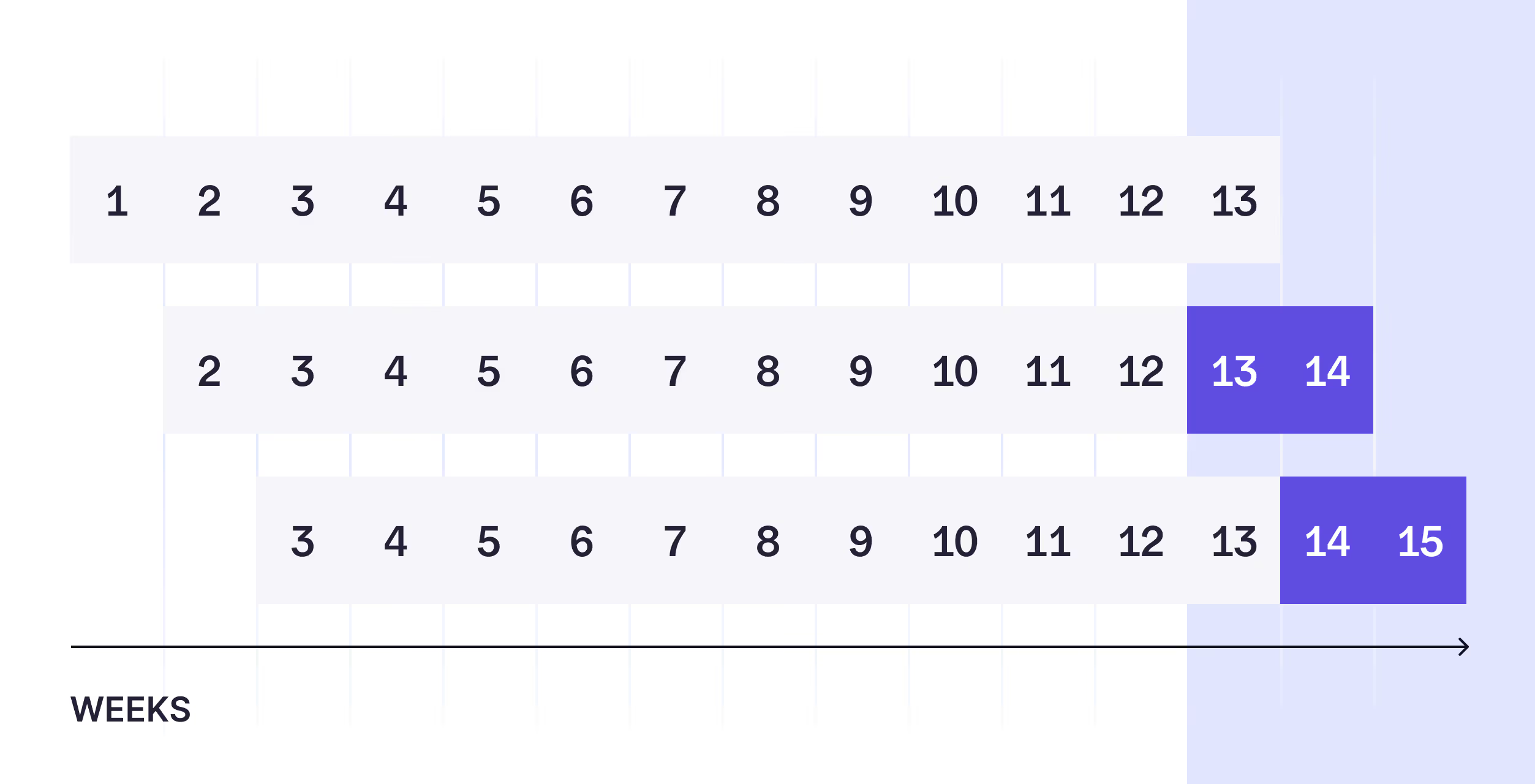

Forecast frequency and updates

Long-term forecasts, such as those covering six months or more, are typically created on a one-off basis—either quarterly or annually—and are intended to support long-term planning. In contrast, a 13-week forecast is used for short- to medium-term planning and is often updated weekly.

A rolling 13-week forecast is widely considered best practice over a static forecast because it provides greater accuracy and real-time visibility into cash inflow and outflow trends. Unlike a static forecast, a rolling forecast is continuously updated with new data, rather than relying on fixed, unchanging information. Although rolling forecasts require more maintenance, automating data collection can greatly reduce the workload.

Why do companies use a 13-week time horizon?

A universal truth of forecasting is that accuracy degrades as forecast range increases. Most companies use a 13-week time horizon for regular cash flow forecasting because it strikes a good balance between accuracy and range. In any case, your time horizon should always be chosen intentionally based on business objectives—it determines the range and depth of information you can feasibly uncover from your forecast, whether that’s daily payments, weekly cash receipts, or quarterly sales trends.

Reliable, accurate insights

The 13-week model is short enough to be reliable because it lets you use historical data and expected transactions to estimate cash flow in the near term. But unlike shorter-term models—think week-to-week forecasting—it still provides a medium-term view for cash planning and decision-making.

Granular level of detail

A 13-week forecast typically consists of weekly reporting periods, as opposed to a consolidated multi-week view. Depending on the tooling used, some 13-week forecasts may provide daily and transaction-level visibility. This granularity lets finance and treasury teams use the forecast to inform their day-to-day activities, such as scheduling supplier payments or planning debt drawdowns, loan repayments, and investments.

Liquidity risk visibility

Since 13-week forecasts offer visibility over a company’s week-to-week liquidity, they enable companies to identify medium-term liquidity risks with a high degree of accuracy. Thirteen weeks is also typically sufficient time for action to be taken to resolve any potential shortfalls, such as by exploring external financing or arranging intercompany loans.

Reporting and planning cycles

With its high level of detail, the 13-week forecast is widely valued as an accurate measure of creditworthiness and financial control. Management teams, along with external creditors, investors, and regulators, often expect an updated forecast on key reporting dates—whether monthly, quarterly, or annually. The 13-week timeframe covers a full quarter and includes the next quarter-end or key reporting date, aligning well with most planning and reporting cycles.

Also, since it’s broken down weekly, unlike most financial plans and budgets that are organized monthly, a 13-week forecast helps prevent short-term planning gaps. This weekly structure offers four times the granularity of month-to-month plans, capturing daily or weekly trends that might otherwise be overlooked.

When is a 13-week time horizon not suitable?

13-week forecasts are not totally ubiquitous—there are times when other forecast models are more appropriate, depending on your forecasting objectives and your company’s business model. Also, some companies use a hybrid model, updating their 13-week forecasts on a weekly basis and their 6-month forecasts on a monthly basis, for example.

Short-term liquidity planning

For businesses focused on immediate liquidity needs, a shorter forecast horizon can be more effective. For example, a 10 or 15-business-day model may be ideal for companies that need to manage lines of credit, high interest rates, and heavy liability. The shorter time horizon gives you the level of detail needed to quickly settle debts, closely manage cash, and plan spending in the very near term.

Long-term liquidity risk management

For a clearer view of longer-term cash needs, a 6-month forecast can be more effective. This approach often involves weekly projections for the first 13 weeks, followed by monthly projections for the next 3 months. Such a setup helps flag potential liquidity risks further down the line—like ensuring there’s sufficient cash to support expansion initiatives.

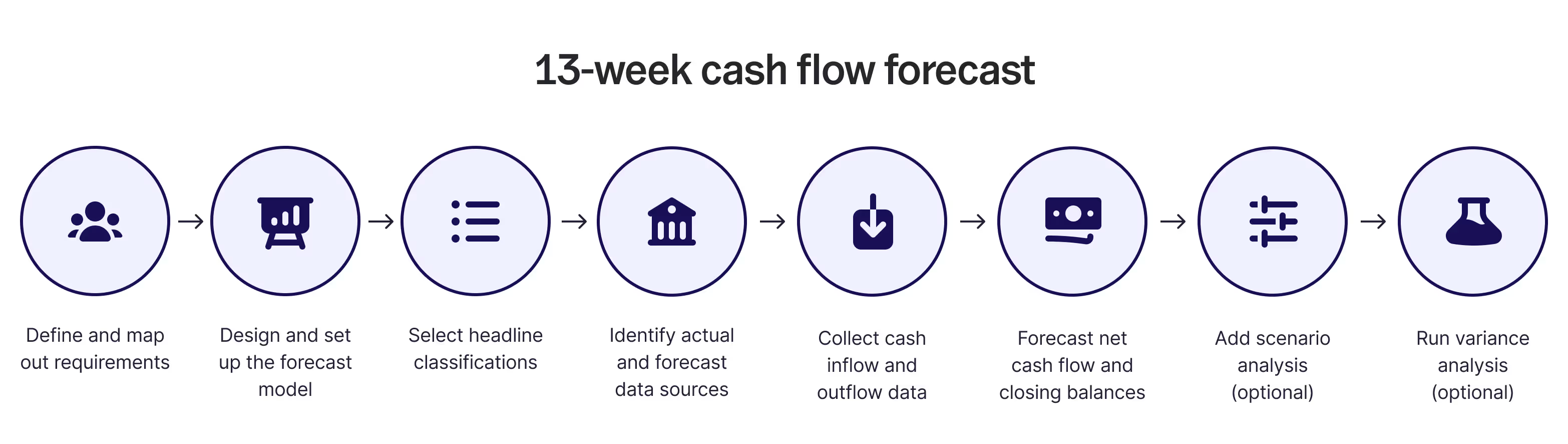

The process to create a 13-week forecast

A 13-week cash flow forecast is a powerful tool for financial analysis and insights, but it can require substantial effort to create and maintain—especially if data collection is done manually. While building the model takes some initial work, the real time commitment lies in continuously gathering, reviewing, and reconciling cash flow data from multiple sources.

Below is an overview of the key tasks involved in setting up a 13-week forecast, with each step covered in more detail. Many of these tasks can be automated using software solutions, such as a treasury system connected to your ERP and other financial tools.

- Map out stakeholder requirements

- Design the 13-week forecast model

- Select your headline classifications

- Identify data sources for actual and forecast cash flow data

- Collect data on cash inflows and outflows

- Forecast net cash flow and closing cash balances

- Incorporate scenario analysis (optional)

- Perform variance analysis (optional)

Map out stakeholder requirements

Begin by identifying your key stakeholders and understanding their primary objectives for the 13-week cash flow forecast, as this will guide its design and functionality. For instance, if day-to-day liquidity risk management is a priority, the forecast should be precise enough to flag potential liquidity issues early, allowing adequate time for action.

Senior management may focus more on using the forecast to drive medium-term cash management plans, such as reducing debt levels and interest costs. To enable this, the forecast should include functionality for easily collecting and consolidating cash positions across the business, ensuring that any pools of excess cash can be identified. Investors, meanwhile, may view the forecast as an indicator of the company’s working capital and overall financial health. They may prioritize the format and frequency of reporting to align with their monitoring needs.

Design the 13-week forecast model

The forecasting model refers to the reporting structure and associated logic that produce the desired forecast output. This model is typically divided into two main components:

- Model dimensions: These define how output data is presented, segmented by reporting periods and reporting categories.

- Input data: The model usually incorporates two types of cash flow data—actual and forecast.

Since this guide is an in-depth review of the 13-week forecast, which typically operates on a weekly frequency, the reporting period is already set as weekly over a 13-week span. With the reporting period confirmed, your focus can turn to exploring reporting categories in greater detail.

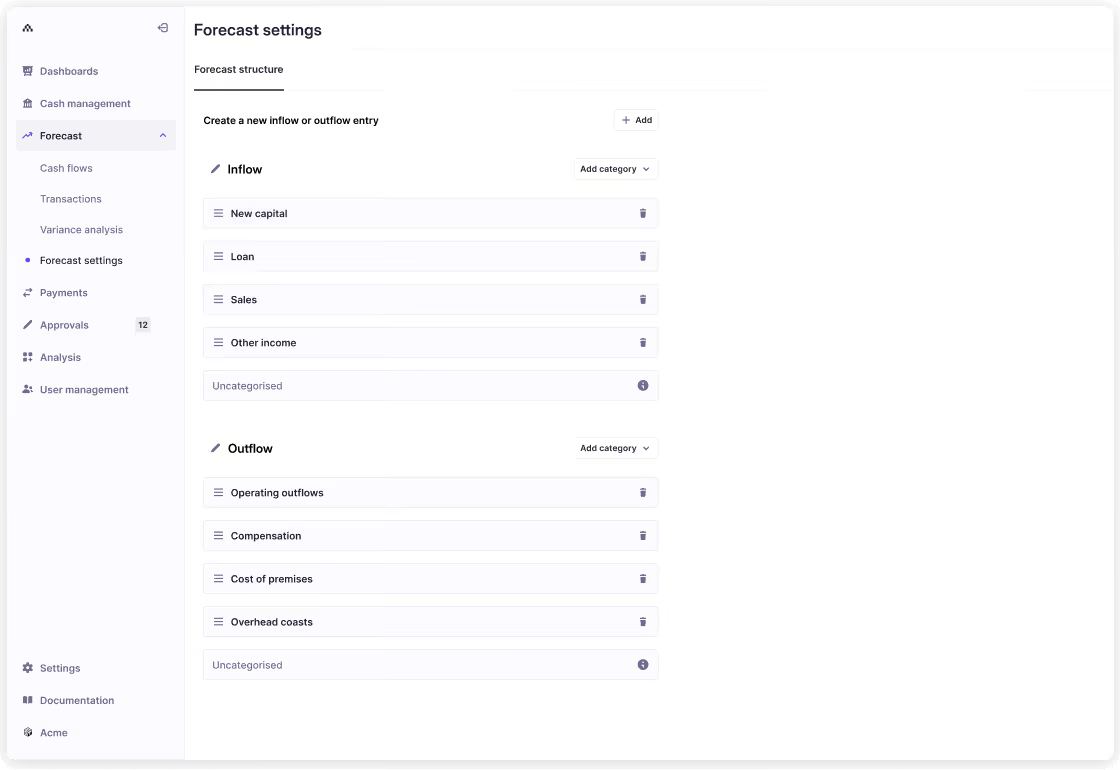

Select your forecast categories

At the highest level, forecasting categories are divided into inflows and outflows. Within these buckets, the classification of categories (or headline groups) and their respective line items should be tailored to your company’s business model and main forecasting objectives. For instance, if capital expenditure is a key area of focus, it could be displayed as a headline under outflows with more detailed line items beneath it.

The level of granularity required in your forecast should be considered from the outset. For example, some businesses may need to see inflows or outflows at the level of individual suppliers or customers. For other businesses, this level of detail could simply obscure the big picture.

Additionally, it’s worth bearing in mind that, unless transactions are automatically tagged and categorized for forecasting purposes, you will need to manually categorize inflows and outflows during data collection on an ongoing basis. Below are a few of the most common headline groups in 13-week forecasts.

Customer inflows

Customer inflows (or customer receipts) are the primary revenue source in most cash forecasts, representing income generated by the core business. The level of detail under this category can vary based on the business model. For instance, companies selling uniform-price items may benefit from a breakdown of units sold by location or channel. In contrast, subscription-based businesses or those with high payment delay risks might structure this line item differently for greater insight.

Supplier payments

Supplier payments, which comprise a significant portion of accounts payable, are categorized based on company setup, data availability, and forecasting needs. For example, if supplier payments vary widely due to factors like asset prices (e.g., iron ore for construction or oil for logistics), grouping these by price-sensitive categories may help forecast trends in tandem with external price changes.

Payroll

Payroll often represents one of the largest and most predictable cash outflows, as salaries are usually consistent and paid at regular intervals. The level of payroll detail depends on forecasting requirements—breakdowns may be by role (e.g., executive, management, support) or by geography or business function, depending on which view best supports decision-making.

Capital expenditure (CapEx)

CapEx forecasting can be challenging, especially if timing depends on external factors outside the company’s control, such as the finalization of a corporate acquisition. How CapEx items are classified may depend on their frequency, with one-off expenses often placed under a "non-recurring" category.

Tax

Tax forecasting complexity depends on tax type, jurisdictions, and industry. A global beverage company, for example, might categorize taxes by geography to account for country-specific alcohol taxes, while a consultancy may categorize by tax type if it incurs various tax obligations based on project types.

Intercompany transactions

Intercompany cash movements can be complex to track and reconcile. Specialized software offers tools for automating intercompany reconciliations, ensuring that transfers net to zero. Without such tools, manual uploads should be carefully structured to reflect movements in both sending and receiving entities.

Debt and interest payments

Debt and interest payments have recently become one of the simpler elements to forecast and categorize, largely due to stable, low interest rates over the past decade. Corporate debt payments are typically negotiated with fixed terms, minimizing unexpected changes. These payments are generally categorized either by lender or debt type.

One-off items

Including a “one-off” category in the forecast helps manage non-regular expenses without creating new line items for each unique transaction. This allows clearer analysis by isolating such expenses and preventing the distortion of recurring trends. For each one-off item, it’s essential to include a note explaining what the item is and why it appears in the forecast.

Identify your cash flow data sources

A 13-week cash flow forecast relies on a variety of data sources, typically categorized as either actual or forecast data—although some sources may provide both. When setting up a forecast, one of the main goals should be to automate data inputs wherever possible.

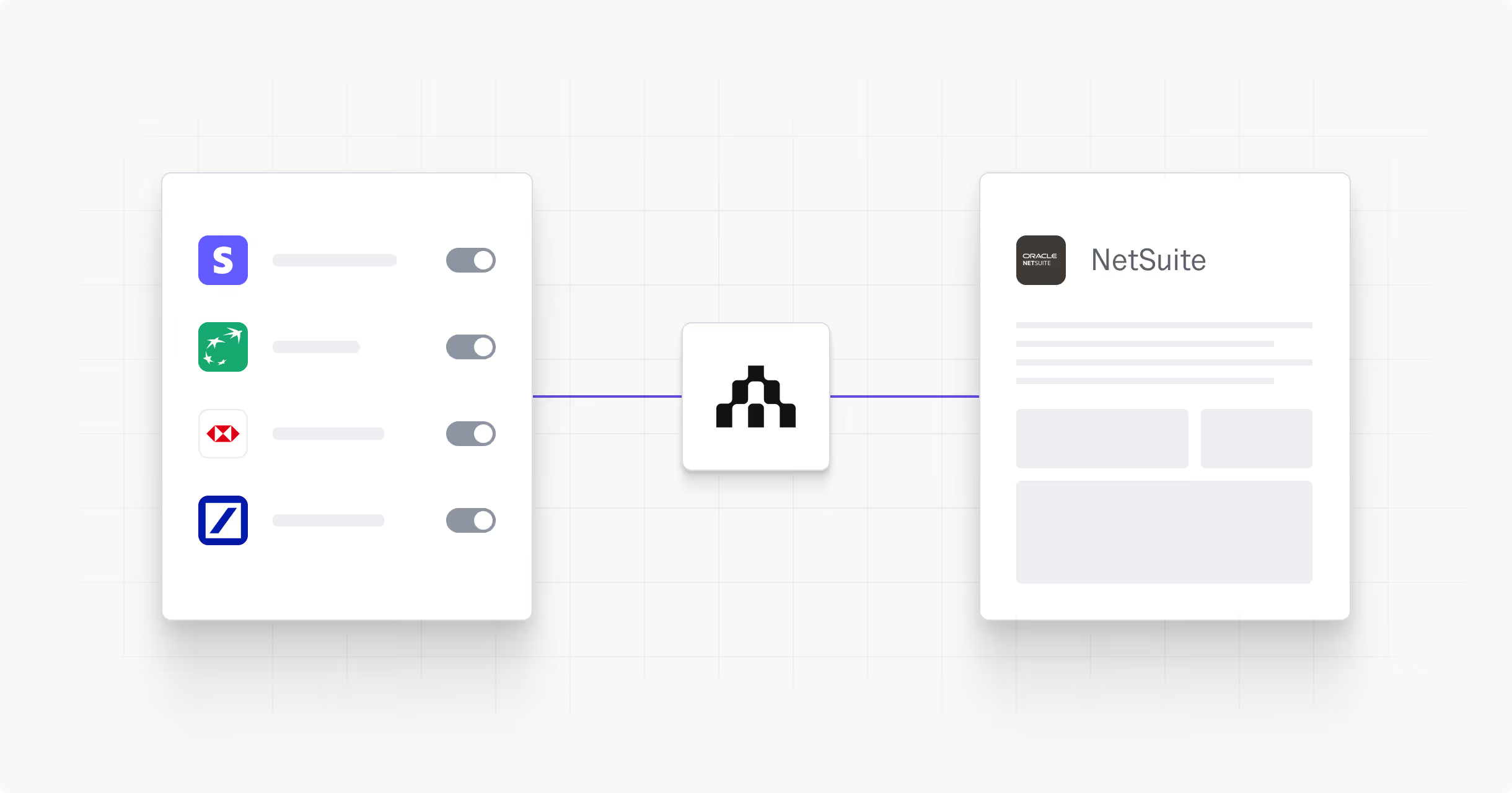

Fully automated data collection is best achieved through a treasury system with forecasting capabilities linked to your ERP, allowing an automated flow of balance data and transactions into the forecast. This is usually done using either an Application Programming Interface (API) or Secure File Transfer Protocol (SFTP) connection that feeds source data into the forecasting model. To learn more, read our guide to bank and ERP connectivity.

Atlar integrates natively with ERP systems such as Oracle NetSuite and Microsoft Dynamics 365 for this very purpose—and connects to over 50 major banks, payment providers, and other financial systems. Browse our live integrations for the latest information.

Actual cash flow data sources

Actual data is essential for cash flow forecasting, as it provides the baseline from which forecasts are projected. Actual cash flow data is also what makes variance analysis possible, letting you gauge the accuracy of your forecast. Without this, it can be difficult to pinpoint causes of inaccuracy for improvement.

Mapping data sources

Depending on the source, a mapping exercise is often required to pre-categorize and group data for the forecasting model. For instance, if transactions are recorded daily, mapping rules will need to consolidate these into weekly data before loading it into the forecast.

Electronic bank statements

Most banks offer electronic bank statements upon request, though they can come in a variety of formats that would need to be standardized before they’re usable for forecasting. The two most common formats are MT940 or BAI2, both of which are standardized to some extent though MT940 can come in structured or unstructured formats. The MT940 format is commonly used in Europe, while BAI2 is preferred in the U.S. Treasury management platforms like Atlar are designed to fetch and standardize this data, regardless of the file format.

ERP and accounting systems

Many organizations use ERP systems like SAP S/4HANA, Microsoft Dynamics 365, or Oracle NetSuite, which include built-in export and integration capabilities. Connecting ERP data to cash forecasting software allows easy access to actual payables and receivables data. Mapping these cash flows to the forecasting model streamlines the forecasting process.

Forecast cash flow data sources

The primary data sources for forecasting cash flow are a company’s accounts payable and accounts receivable. However, this information is typically spread across multiple systems and departments at the company. Different data sources may be used for individual reporting categories within the forecast, as well as for the same categories across various time horizons (from short to long term).

Streamlining data collection

Since forecast data is often not centralized in one system, it’s essential to automate this process as much as possible; otherwise, ongoing forecast updates can become very time-consuming. Where automation isn’t feasible, collecting forecast data may require manual inputs from one or more planning departments. In these cases, establishing a clear process for regular communication with other teams is key.

ERP systems

ERP systems generally hold forward-looking data on accounts payable and receivable, but typically only for a relatively short time horizon. Since most systems have built-in export and integration functionality, it should be possible to automate the data feeds into your forecasting tool.

Financial planning and analysis (FP&A) tools

Financial planning tools, whether standalone or integrated into an ERP, typically store data that is valuable for forecasting over a medium- to long-term time horizon. Most FP&A systems have data export capabilities, making it relatively straightforward to integrate them with your forecasting process.

People

Input from people across business units often helps to refine a cash flow forecast while also improving its accuracy significantly. Manual input processes can add complexity and delays—though some software tools simplify this by allowing employees to input data directly into a centralized system.

Collect your inflow and outflow data

Once you’ve identified your data sources, the process to actually collect the data is what typically takes the most time on a recurring basis. At a high level, it involves exporting data from multiple systems, reviewing it and potentially reconciling it against your bank statements, standardizing the data to fit your forecast model, and correctly importing it into the model itself.

This process may also require a degree of manual number-crunching. For instance, you may need to review historical data and use sales or accounts receivable forecasts to estimate when and how much cash will be received weekly—while adjusting for seasonality or customer payment trends that could impact the timing of specific inflows.

Similarly, for cash outflows, you may need to manually break expenses down into weekly amounts based on payment schedules, while also considering any periodic payments that fall within the 13-week period (such as monthly payroll or quarterly taxes).

Forecast your net cash flow and closing cash balances

This step in the process involves calculating your net cash flow on a weekly basis and then combining it with your starting cash balance to arrive at your forecasting closing balance for each week in the forecast. Here’s a simplified overview:

- For each week, calculate the net cash flow by subtracting total cash outflows from total cash inflows.

- Next, determine the starting cash balance for the forecast period. This should typically be reconciled with your bank statement(s) to ensure accuracy.

- For each subsequent week, take the net cash flow and add it to (or subtract it from) the opening balance of the previous week.

- This gives you the closing cash balance for each week of the forecast period.

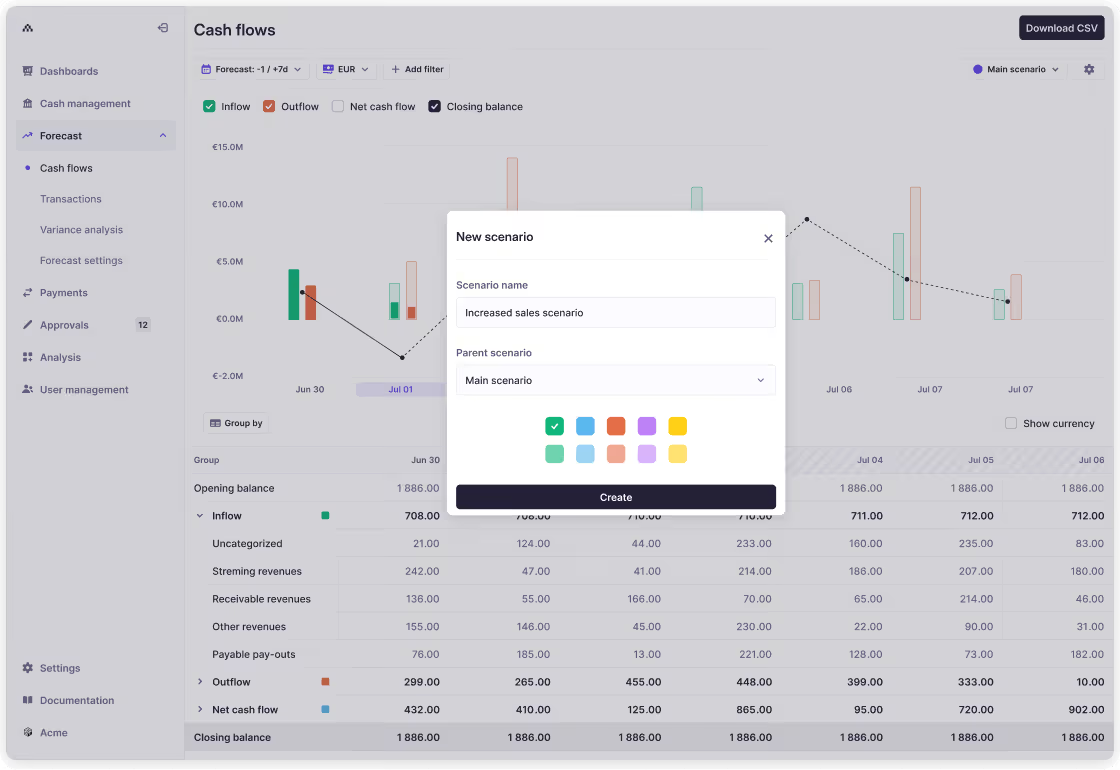

Incorporate scenario planning

Scenario planning involves creating different projections (or scenarios) to simulate potential cash flow outcomes based on various assumptions. For a 13-week cash flow forecast, scenarios might include best-case, worst-case, and baseline cases, each reflecting different factors such as revenue changes, unexpected expenses, or shifts in payment timings.

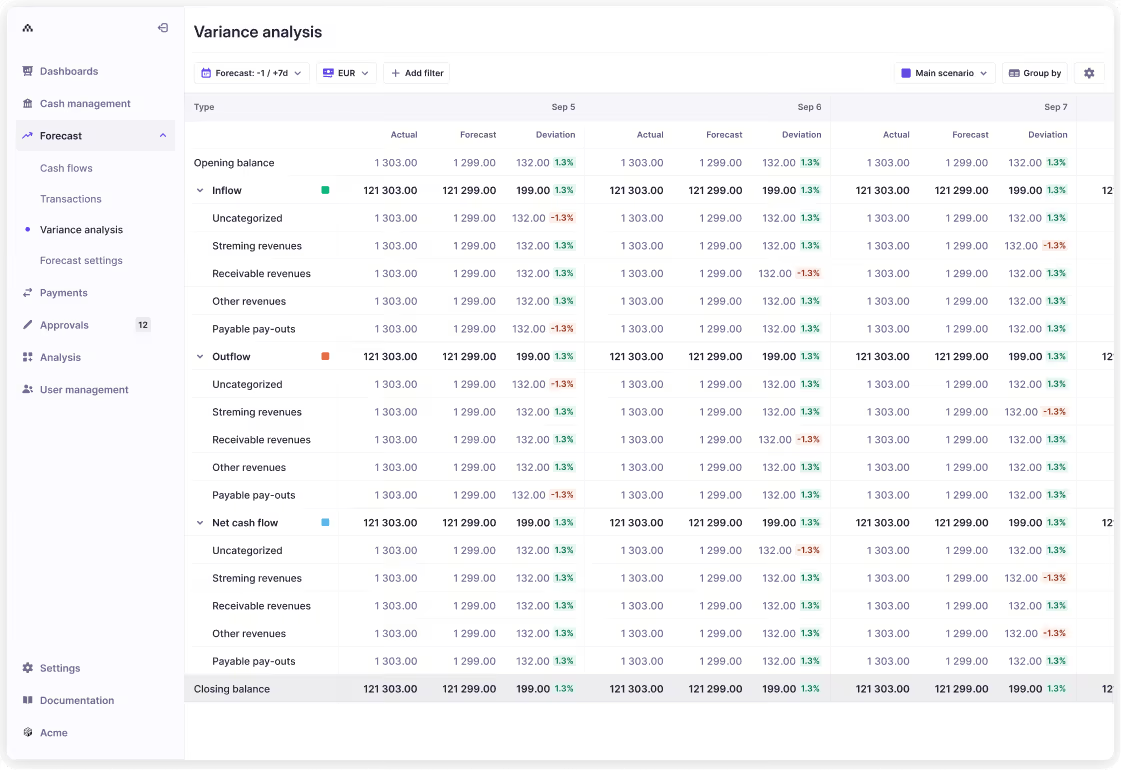

Perform regular variance analysis

Variance analysis compares forecasted cash flows with actual cash flows to measure the accuracy of the forecast and improve its reliability over time. Typically performed on a weekly basis, it often helps finance teams to identify specific factors causing forecast inaccuracies, such as late customer payments or unanticipated expenses.

The different types of cash flow forecasting tools

As mentioned earlier, several of the most time-consuming steps in the forecasting process can be automated—provided you have the necessary software tools in place and an easy way of streaming data between them.

Spreadsheets and business intelligence tools

When using spreadsheet software like Microsoft Excel or Google Sheets, or business intelligence (BI) tools, forecasts are created manually and customized to specific needs. However, these tools don’t integrate directly with banks or ERP systems, so data must be entered manually or imported as a CSV file or similar, often requiring formatting adjustments to ensure compatibility.

- Advantages: Highly customizable, familiar to most users, and low initial set up cost aside from the time investment.

- Disadvantages: Labor-intensive and error-prone due to manual inputs, with limited scalability for complex forecasting needs like scenario planning and variance analysis. The lack of automatic updates results in outdated insights and makes implementing a rolling forecast more challenging.

ERP systems with a forecasting module

ERP systems like SAP S/4HANA or Oracle NetSuite offer optional forecasting modules that leverage data from the ERP’s existing accounts payable (AP), accounts receivable (AR), and general ledger systems. However, these modules often have limited reporting and analytics capabilities compared to specialized tools, and they require integration with banks to incorporate external bank data into the forecast.

- Advantages: Centralized within the ERP system and uses existing financial data for consistency and accuracy.

- Disadvantages: Limited flexibility and forecasting depth compared to specialized tools, and integrating external bank data or reconciling intercompany cash flows can be challenging. Bank-ERP integrations often become costly projects, which may not justify the investment if used solely for forecasting purposes.

Dedicated cash flow forecasting software

Specialized platforms that focus primarily on cash flow forecasting tend to offer rich functionality like advanced modeling, scenario planning, and reporting features. These tools may be able to integrate directly with banks and ERP systems but often require third-party connections or custom setups.

- Advantages: Advanced forecasting capabilities with robust analytics—ideal for organizations with complex forecasting needs that may extend beyond the 13-week cash flow forecast.

- Disadvantages: Specialized forecasting tools are standalone systems that require separate integrations and data feeds, leading to more IT work, higher costs, and potentially a duplication of efforts. These tools are typically ineffective for broader treasury management needs.

Treasury software with built-in forecasting

Many treasury platforms offer fully integrated forecasting tooling alongside other cash management functionality, such as Atlar’s cash flow forecasting product. Designed to connect with banks and ERP systems, treasury systems help automate data collection and provide end-to-end cash visibility across your financial ecosystem, including banks, ERP, and potentially other finance tools.

A key advantage of using treasury software for forecasting is the reduced reliance on multiple standalone tools with specialized use cases. With one platform, you can manage payments, cash forecasting, and broader cash management processes, delivering higher ROI compared to the initial software cost.

- Advantages: Automated data updates, potentially in real time, for accurate and timely forecasts with less manual effort. Centralizes cash management, forecasting, and liquidity planning in one system—ideal for businesses looking for scalable treasury operations.

- Disadvantages: Higher upfront cost compared to spreadsheets or basic ERP modules.

How Atlar helps with 13-week forecasting

Atlar customers Storytel, Aiven, Zilch, and Upvest have partnered with us to seamlessly integrate their banks and ERP systems, transforming their treasury operations—cash flow forecasting included. Atlar’s 13-week cash flow forecasting feature automates the heavy lifting, enabling finance and treasury teams to focus on analysis and strategic cash planning. Below are some of the key ways Atlar enhances your 13-week forecasting process.

Automated bank and ERP data collection

With native integrations to ERP systems like Oracle NetSuite and Microsoft Dynamics—plus over 50 integrations with major banks—Atlar seamlessly connects and standardizes all financial data into one platform, automating the collection of actual and forecast cash flow data. This eliminates the need for manual data entry, file uploads, and reconciliation, ensuring your 13-week forecast is always up to date. With data flowing directly into Atlar, finance teams can spend less time gathering information and more time analyzing cash positions.

Custom categories and transaction tagging

Atlar’s forecasting tool allows you to set up custom forecast categories and automatically tag transactions as Atlar receives them, mapping them to the appropriate forecast categories. Whether it’s different revenue types, customer receipts, payroll, or supplier payments, Atlar ensures every transaction is classified correctly according to your preferred reporting structure—streamlining the forecasting process and minimizing inaccuracies.

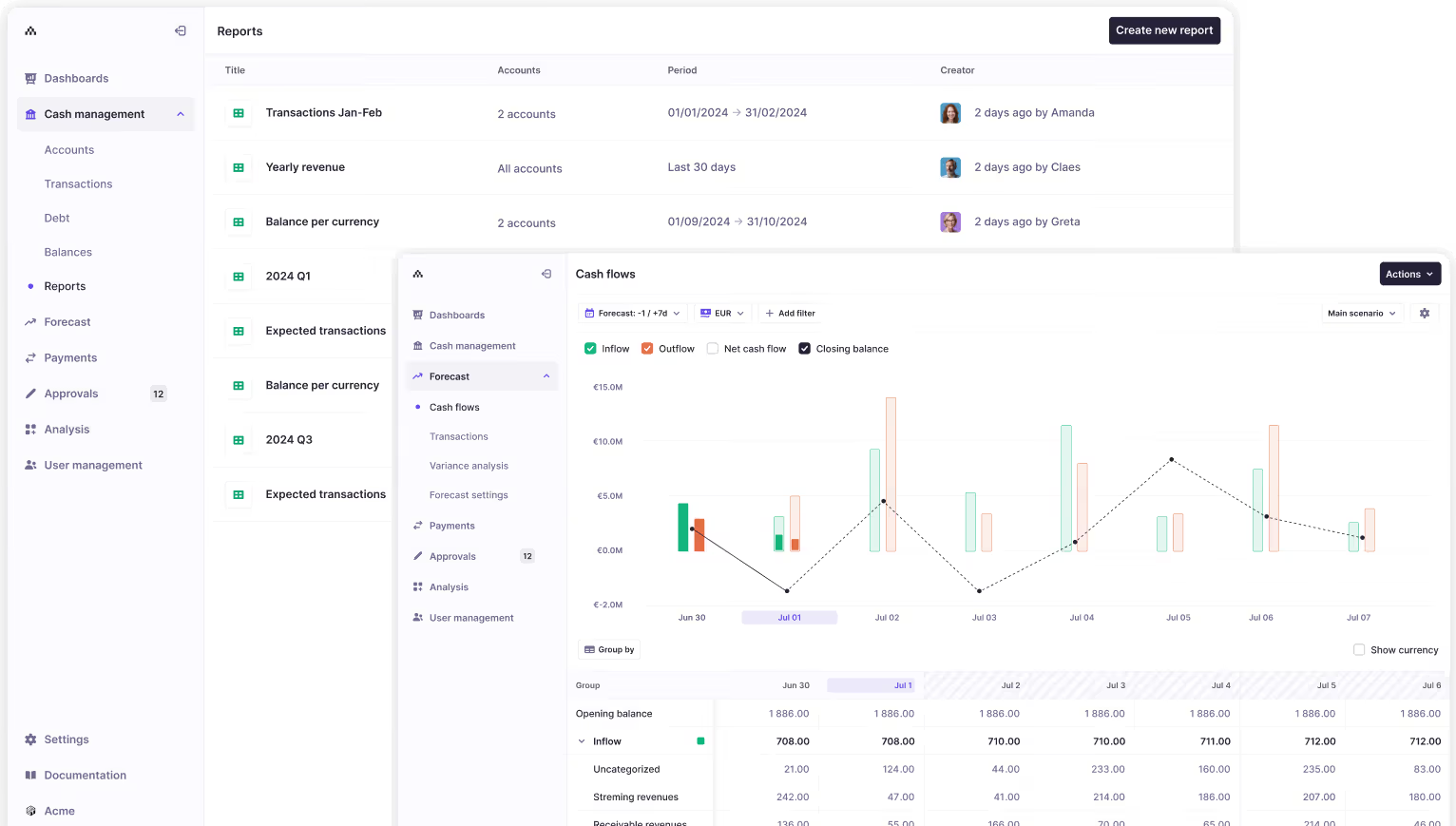

Intuitive, user-friendly forecasting tools

Designed with modern UX principles in mind, Atlar’s reporting tools make it easy to track and analyze cash flow trends. With a clean, simple interface, you can drill down into specific weeks, identify variances, and quickly visualize cash positions across all of your banks and accounts. You can also create custom reports and dashboards, so stakeholders can see the insights relevant to them.

Rolling 13-week forecasts in real time

Atlar’s 13-week forecast updates automatically as new data becomes available. Since Atlar is able to support real-time API connections with your financial partners, this means your forecasts can be updated in real time—ensuring you always have an accurate, forward-looking view of cash inflows and outflows.

Built-in scenario planning and variance analysis

With Atlar, you can easily model different cash flow scenarios—optimistic, pessimistic, or baseline—directly within the platform. Built-in variance analysis tools let you compare forecasted and actual cash flows, helping to refine your forecasts and improve accuracy over time.

See Atlar's forecasting tools in action

Looking to improve your forecasting processes? Atlar offers user-friendly forecasting tools to help you get started with a rolling 13-week forecast in a matter of minutes—so you can focus your time on analysis and decision-making. If this sounds interesting, book a 30-minute demo with our team to see Atlar’s forecasting capabilities at work.

You can unsubscribe anytime.

Most recent

See Atlar in action.

Enter your work email to watch a live product demo.