Bank Reconciliation: A Practical Guide for Finance and Accounting Teams

Reconciliation is a key process in accounting and treasury management that involves comparing two sets of records to make sure they match. For example, you might compare your company’s internal transaction logs to an external document (like a vendor invoice or a bank statement) to confirm that both show the same amounts and dates for each transaction.

When you perform a reconciliation, you are looking for discrepancies—differences in amounts, missing transactions, or timing mismatches. Identifying and resolving these ensures that your financial reports are reliable. This, in turn, builds trust with stakeholders—whether they are company executives, auditors, regulators, or investors.

This guide zeroes in on bank reconciliation specifically, which is one of the most common and essential forms of reconciliation, alongside accounts receivable (AR) and accounts payable (AR) reconciliation.

At Atlar, we help many of our customers to streamline bank reconciliation through full bank-ERP connectivity and automated bank feeds. In fact, Atlar is an official NetSuite partner and offers native integrations with other major ERP systems like Microsoft Dynamics 365 and SAP S/4HANA. To learn more about our solution, get in touch with our team.

What is bank reconciliation?

Bank reconciliation is the process of comparing your internal records of cash transactions—often referred to as a cashbook or cash ledger—with the transactions listed on your bank statement for a specific period. The goal is to ensure all transactions are accounted for accurately and to spot any discrepancies.

In practice, it involves matching records from your bank statement (or another cash account statement) with transactions that have already been posted in your ERP, general ledger, or main accounting record. You take a payment from your bank statement and match it with a specific bill, invoice, or chart of accounts (COA) document.

By routinely matching these two records, you ensure that your company’s reported cash balance is truly accurate. If there are differences, you investigate the cause and correct them as needed. This helps avoid overdrawn accounts, missed transactions, or unnoticed fees. Bank reconciliation typically covers:

- Money going out, or cash outflows (e.g., outgoing payments to suppliers, payroll, loan repayments)

- Money coming in, or cash inflows (e.g., customer payments, interest received, refunds)

- Bank charges (e.g., monthly account fees, foreign exchange fees, overdraft costs)

Bank reconciliation is most commonly performed using bank statements, but not always. As companies increasingly use other systems to send and receive payments, such as online payment platforms, there is a need to apply the same reconciliation process to the cash processed in these systems too.

What is a cashbook?

Bank reconciliation is the act of comparing your bank balance to the balance in your cashbook, cash ledger, or accounting record. A cashbook is a record of your cash receipts and payments, tracking deposits and withdrawals, and is essentially a subsidiary ledger (or day book) dedicated to cash transactions. The balance in your cashbook may also be referred to as your book balance.

The detailed entries in your cashbook are typically summarized and posed to your general ledger, which holds the main accounts for all financial transactions, including (but not limited to) cash, accounts receivable, accounts payable, and equity.

The form your cashbook takes, and where it’s stored, depends on the accounting or ERP software you’re using and may also be referred to as a “cash register” or “bank register.”

Why bank reconciliation is important

Bank reconciliation is essential for safeguarding the accuracy of your financial data and improving decision-making. A key task within accounting, it’s often performed as part of the month-end close process. According to the Association of Certified Fraud Examiners, around 22% of financial statement fraud cases are uncovered through bank reconciliation, highlighting its importance in preventing fraud.

Here are the main reasons to perform bank reconciliation:

Accuracy

Regular bank reconciliations help ensure your financial records match your bank statements, reducing the risk of reporting inflated or understated balances. This is vital for preparing reliable financial statements and making business decisions. If you need external financing, having clean, accurate financial statements can also speed up due diligence and build trust with lenders or investors.

Fraud prevention

By comparing your records with bank statements, suspicious activity such as unauthorized transactions, repeated errors, or other discrepancies can be detected early.

Managing cash flow

Accurate bank reconciliations provide a clear picture of your cash flow, confirming you have sufficient funds for your operations and investments and making it easier to plan and invest.

Compliance

Regular bank reconciliation helps you comply with accounting standards and regulations by ensuring your records are accurate and up-to-date. In Europe and North America, mid-sized and enterprise companies often follow the International Financial Reporting Standards (IFRS) or Generally Accepted Accounting Principles (GAAP) respectively. Bank reconciliation is a key part of fulfilling these standards.

How to perform bank reconciliation(s)

The type and frequency of bank reconciliation a company needs depend on factors like transaction volume, business complexity, and regulatory requirements. Companies with high transaction volumes, multiple bank accounts, or international operations often require more frequent reconciliation, especially if they handle multi-currency transactions or rely on SEPA, SWIFT, or card payments.

Businesses with tight cash flow margins or a higher risk of fraud may also need more frequent checks, while those with lower transaction volumes or strong automation can reconcile less often with minimal effort.

Locate your bank statements and cashbook

Cashbooks typically reside in your accounting or ERP system, while bank statements come from the bank, either physically or online.

Where to find the cashbook:

- In accounting software: Look for something labeled as a “cash register,” “bank register,” or “cashbook” under your “Chart of Accounts” or “Banking” section. This is where all your cash transactions are recorded.

- In an ERP system like NetSuite or SAP: The cashbook might be embedded as a subsidiary ledger in a financial module. You’d typically access it via a financial accounting or general ledger submenu.

- Manual spreadsheet-based systems: If your organization is using spreadsheets, you might have a dedicated “cashbook” tab specifically for recording receipts and payments.

Where to find bank statements:

- Online banking portal: Many businesses download statements directly from their bank’s website or receive them via email.

- Physical statements: If your bank mails paper statements, they’ll be filed in the finance or accounting department.

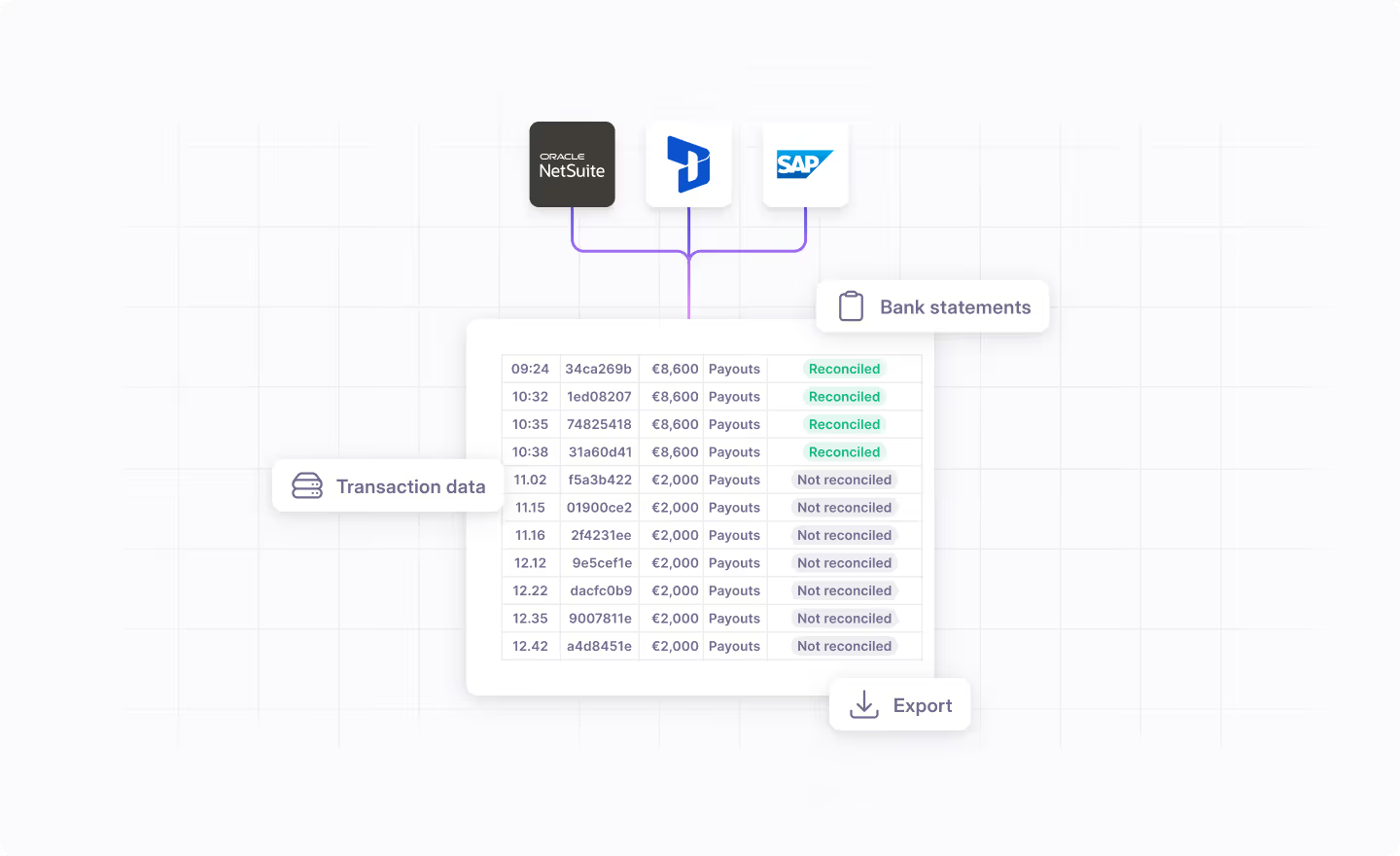

- Integrated bank feeds: Bank-ERP connectivity solutions, like Atlar, allow you to automatically feed transaction data from bank statements into your ERP.

In addition to your cashbook and bank statements, you may want to gather any related payment records—such as invoices, payment confirmations, or receipts—that can help clarify or support your transactions.

Perform the bank reconciliation

Once you’ve gathered all your bank statements for the period you’re reconciling and confirmed your records are complete and up-to-date, the process is as follows:

- Compare opening balances: Check the bank statement’s opening balance and confirm it matches both the closing balance from the previous reconciliation and your internal cashbook or ledger. If there’s a mismatch, you may need to investigate the closing of the previous period first.

- Identify deposits in transit: Deposits in transit are amounts you’ve recorded in your ledger but which haven’t yet appeared on your bank statement. This often happens if you’ve made a deposit just before the bank’s cut-off time. Note these as legitimate timing differences, and carry them forward to the next period if they remain outstanding.

- Spot outstanding payments: Outstanding payments occur when you’ve issued a payment that the bank hasn’t processed yet. If a payment hasn’t cleared for a long time, investigate whether it was lost or canceled.

- Account for bank fees, charges, and interest: Monthly service charges, foreign exchange fees, or transaction fees may appear on the statement but not in your ledger, and so may need to be recorded.

- Match the transactions and investigate discrepancies: Match the transactions recorded in your company's books with those in the bank statement. Entry errors, such as duplicated or missing transactions, should be adjusted immediately. In the unlikely event that there are fraudulent or unauthorized transactions, you should alert your bank immediately.

- Make adjusting entries: Once you identify legitimate differences—like bank fees or unrecorded deposits—create journal entries in your accounting system to align your ledger with the statement.

- Confirm final balances: After all adjustments, your ledger’s ending balance should match your bank statement’s closing balance. If they still don’t match, re-check each stage until you find and resolve the discrepancy.

Adjust discrepancies

There are several reasons you might find a discrepancy between your internal books and your bank statements such as fees charged by your bank or interest earned. Once you’ve indentured these, you’ll need to adjust the statement and book balance. The final result is known as your adjusted bank statement and adjusted book balance.

Bank-ERP reconciliation

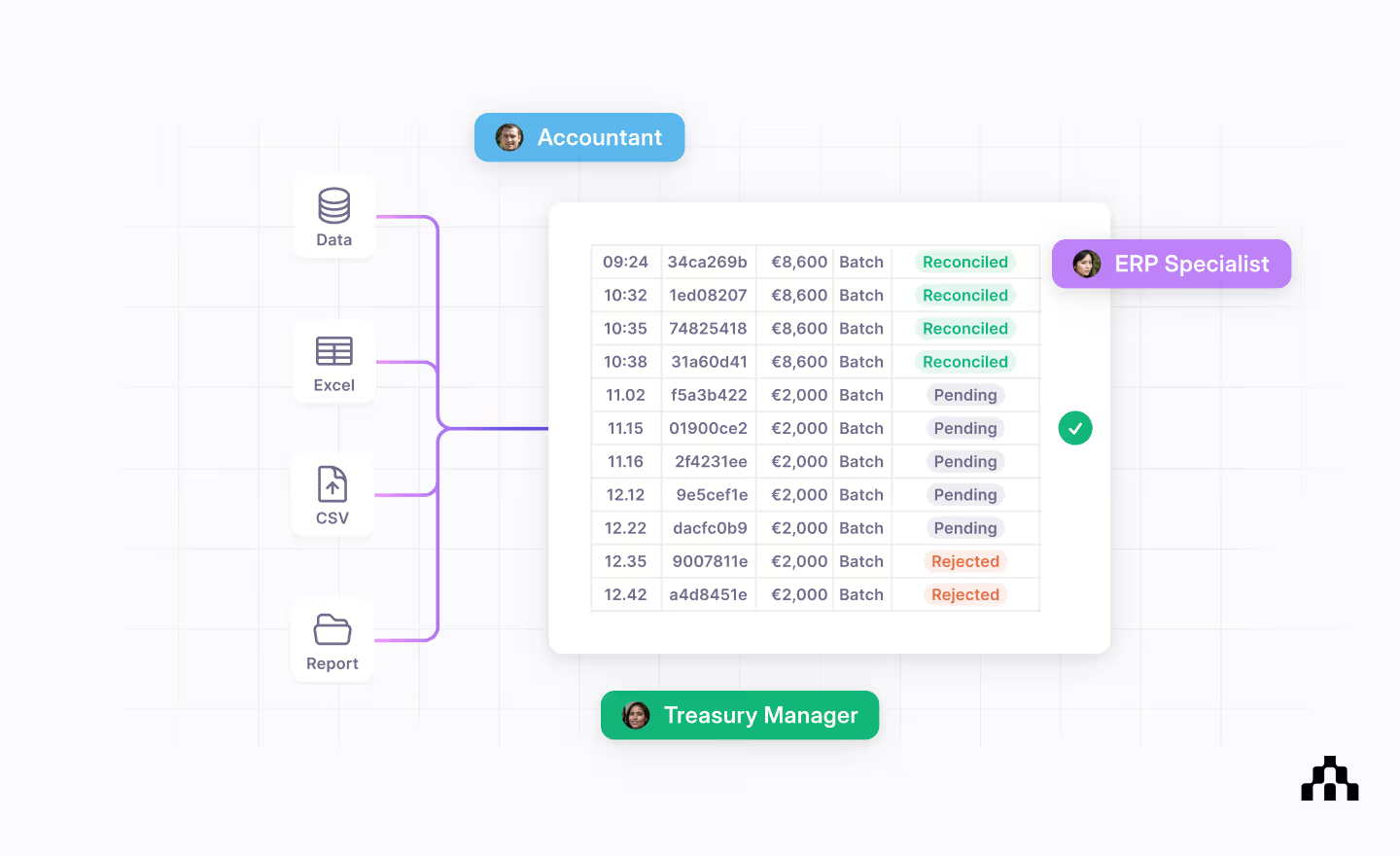

Many companies with a higher volume of transactions choose to invest in ERP software with a general ledger module, enabling them to centralize their transaction data in a single source of truth. Traditionally, companies that use ERP software upload their bank statements, or bank feeds, into their ERP system and match the transactions manually line by line.

The typical process is as follows:

- Retrieve your bank feeds by manually logging into all of your banking and payment portals.

- Format the bank data so it meets the requirements of your ERP system.

- Upload the bank feeds to your ERP system.

- Match ERP transactions with your bank statements line by line and investigating and resolving any discrepancies.

It may be possible to connect your ERP directly to your banks in an effort to automate some of this process. However, since ERP systems are not specialized in building and maintaining bank connectivity it often requires extensive in-house engineering work and the connections will need to be maintained over time. For more information, head to the ERP treasury module section of our in-depth guide to treasury systems.

Example of bank reconciliation in action

Here's an example to illustrate bank reconciliation in practice. In this instance, you start by comparing your bank statement with your book balance, meaning your cash balance according to your accounting records:

- Bank statement: €5,000

- Book balance: €4,500

After comparing the records, you find the following discrepancies:

- Outstanding withdrawals: €600

- Outstanding deposits: €400

- Bank fees: €50

You will need to review and adjust your bank statement and internal records to account for these discrepancies, giving you your adjusted (or calculated) bank balance and book balance respectively.

Adjusting the bank statement

- Bank statement: €5,000

- Minus outstanding withdrawals: €600

- Plus outstanding deposits: €400

- Adjusted bank balance: €4,800

Adjusting your records

- Book balance: €4,500

- Minus bank fees: €50

- Adjusted book balance: $4,450

As you can see, the adjusted balances don’t match. This means you’d need to investigate further to reconcile the €350 difference. The aim of bank reconciliation is to identify all discrepancies and adjust your records accordingly until the difference between the adjusted bank balance amount and the adjusted book balance amount equals zero.

Pitfalls in bank reconciliation (and how to avoid them)

Bank reconciliation can be complex and time-consuming, especially if you have a high volume of transactions and insufficient tooling. Below are some common challenges and how you can avoid them.

Timing differences

The timing of the transactions recorded in your company’s books might not match the processing times of your bank. These discrepancies can be classified as normal timing differences and marked as “cleared” during the following reconciliation.

Manual errors

Errors in data entry or recording transactions can lead to discrepancies. For example, your accounting team might have recorded the same vendor payment twice by mistake. Accurate record-keeping, combined with smart accountancy tools, is essential to minimize these errors.

Bank errors

Although less common, these do happen so you have to be vigilant when going through your bank statements. If you spot an error on the bank’s side, reach out to them for a correction.

Unrecorded transactions

Transactions such as bank fees, interest, and payments might not be recorded in your books straight away. Ensure all information is included, even if the deposit or withdrawal is still outstanding.

Best practices for bank reconciliation

Effective bank reconciliation is not just about matching transactions—it’s about ensuring accuracy, efficiency, and strong financial controls. Below are some best practices to help streamline the process, reduce errors, and gain a clearer view of the company’s cash position.

Automate where possible

Many small companies start with spreadsheets or templates to compare bank statements with their ledgers. While this is simple, it can be time-consuming and prone to human error.

Modern treasury systems, like Atlar, are designed to integrate with both your banks and ERP system and push bank statements automatically (via direct feeds) into your cash ledger. This lets you automatically match transactions and flag discrepancies inside your ERP, which is especially helpful for higher transaction volumes or multi-currency operations. To learn more, read our guide to bank-ERP connectivity.

Reconcile frequently

While monthly reconciliation is a minimum standard for most mid-sized companies, many teams with higher transaction volumes do it weekly or even daily. This makes discrepancies easier to spot and fix before they compound.

Segregate duties

Where possible, separate the roles of those who record transactions from those who reconcile and approve them. This is a foundational internal control that reduces the risk of errors and fraud.

In most companies, the accounting department oversees the general ledger and is responsible for ensuring that all cash transactions—deposits, withdrawals, and bank fees—are accurately recorded in the books. AP and AR teams may handle specific tasks related to outgoing payments (AP) and incoming payments (AR) while, at some companies, the treasury department may also perform or review bank reconciliations.

Keep detailed documentation

Good record-keeping ensures that you can back up the adjustments you make. It’s useful for both internal and external audits, as well as for learning from past mistakes.

Use a standard operating procedure (SOP)

Set up a concise SOP for your bank reconciliation process. This can include:

- Assigned roles: Who gathers documents? Who matches records?

- Deadlines: When must the reconciliation be completed?

- Approval workflow: Who reviews and signs off on the final statement?

How Atlar can help with your bank reconciliation

A well-executed bank reconciliation isn’t just about checking boxes. It plays a vital role in ensuring financial accuracy, preventing fraud, and establishing a clear understanding of a company’s cash position. For most mid-sized and larger companies, it’s a critical process that’s worth investing in.

If you find you’re spending too many hours each month manually comparing spreadsheets and bank statements, it may be time to consider automated solutions that can handle the heavy lifting—so you can focus on more strategic, value-added tasks.

Thanks to native integrations with ERP systems like Oracle NetSuite and Microsoft Dynamics 365 Business Central, Atlar enables its customers to greatly simplify bank reconciliation. In fact, Atlar is an official NetSuite partner and works closely with other major ERP systems.

This enables Atlar customers to automatically import bank statements from any bank directly to their ERP system, removing the need for manual imports. This can be done with any bank connected to Atlar, enabling customers to reliably sync financial data between their banks and their ERP.

Customers can also simplify payment runs by automatically paying vendor bills from their ERP directly in Atlar—with all transaction data fed back into your ERP system, streamlining reconciliation. This lets customers avoid having to manually enter payments in one or more online banking portals. To learn more, explore our accounts payable feature page or get in touch with our team.

You can unsubscribe anytime.

Most recent

See Atlar in action.

Enter your work email to watch a live product demo.